2021 Set for Record Year – Brings Long Awaited $1Trillion Annual Green Milestone Into Sight- Social & Sustainability Growth adds Extra Spice

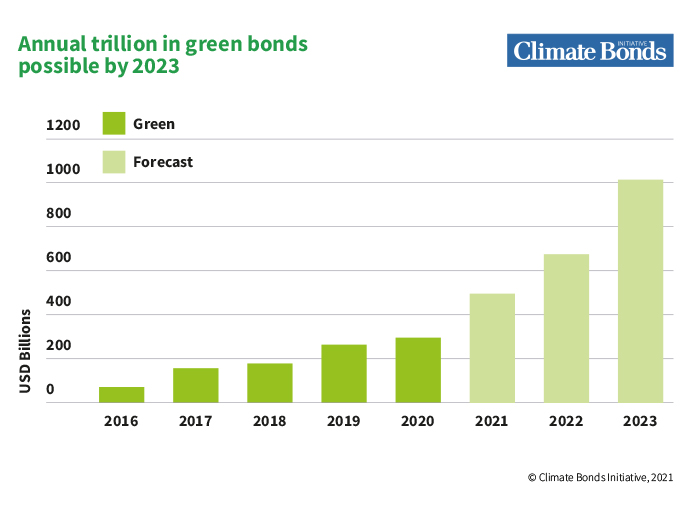

On track for a record $500bn green in 2021

Climate Bonds has lifted its January forecast of USD400-450bn in annual green bond investment to the Half Trillion mark for 2021, reflecting the strength of the green market in the first 6 months of the year.

Green investment for H1 reached USD227.8bn, a very encouraging result when compared to the full 2020 total of USD297bn.

Projections see the long-awaited Milestone of $1Trillion in annual green investment now in sight for 2023.

GSS H1 highlights – a record-breaking half-year

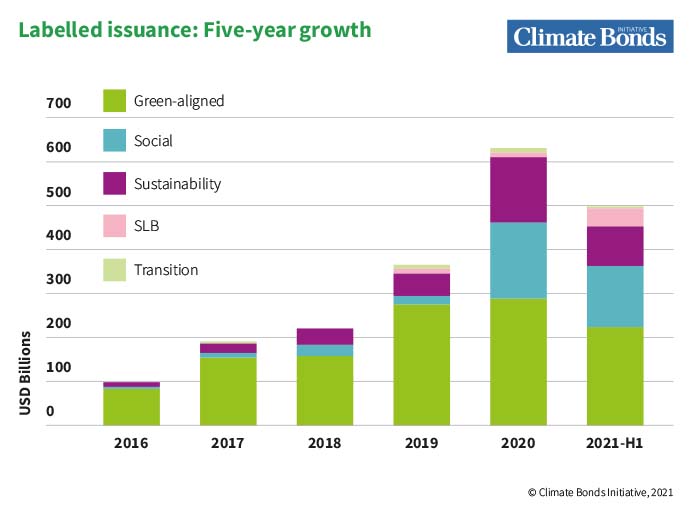

Total volumes for labelled Green, Social and Sustainability (GSS) bonds, Sustainability-linked bonds (SLB) and Transition bonds reached nearly half a trillion (USD496.1bn) in the first half of 2021.

This amount represents 59% year-on-year growth in the GSS market from the equivalent period in 2020. It also sets the labelled sustainable debt market on track to reach another record high by the end of December.

Cumulative labelled issuance now stands at USD2.1tn at end H1 2021.

At a Glance - Green bond issuance

Issuance of green debt instruments continued to grow in the first half of 2021, with volumes included in the Climate Bonds Green Bond Database in this period more than doubling to USD227.8bn compared to COVID-19 Impacted H1 2020 (USD91.6bn) – a record for any half-year period since market inception in 2007.

At USD227.8bn for the first half of this year, green issuance is more than three-quarters (76%) of the full-year 2020 volume of USD297bn, and is past halfway of our original 2021 forecast of USD400-USD450bn. This huge acceleration brings total cumulative green bond volume to USD1.3tn.

Green bonds have been soaring at a 49% growth rate in the five preceding years before 2021. Our analysis suggests that the green bond market annual issuance could exceed the USD 1trillion mark by 2023, even if we are to see a more modest growth rate.

National Rankings

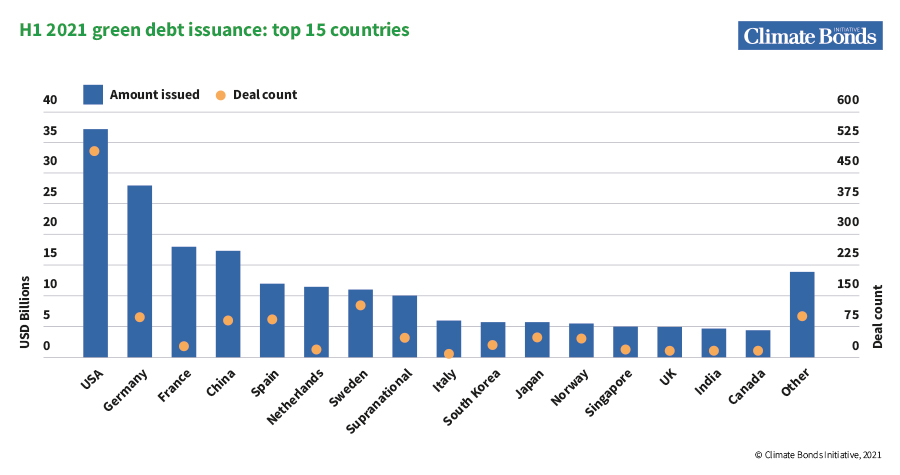

US issuers constituted the largest share of issuance by volume (17% or USD37.6bn) and number of deals (495), Germany placed second with USD28.5bn (13% of issuance volume) and 102 deals.

France and China took the third and fourth spots, with similar volumes (USD22.8bn and USD22bn, respectively, each representing 10% of issuance) but a different number of deals (20 and 92, respectively).

Spain rounded out the top 5, with USD11.7bn (5%) and 34 deals. In total, issuers from 47 countries (excluding SNAT) executed deals in H1 2021.

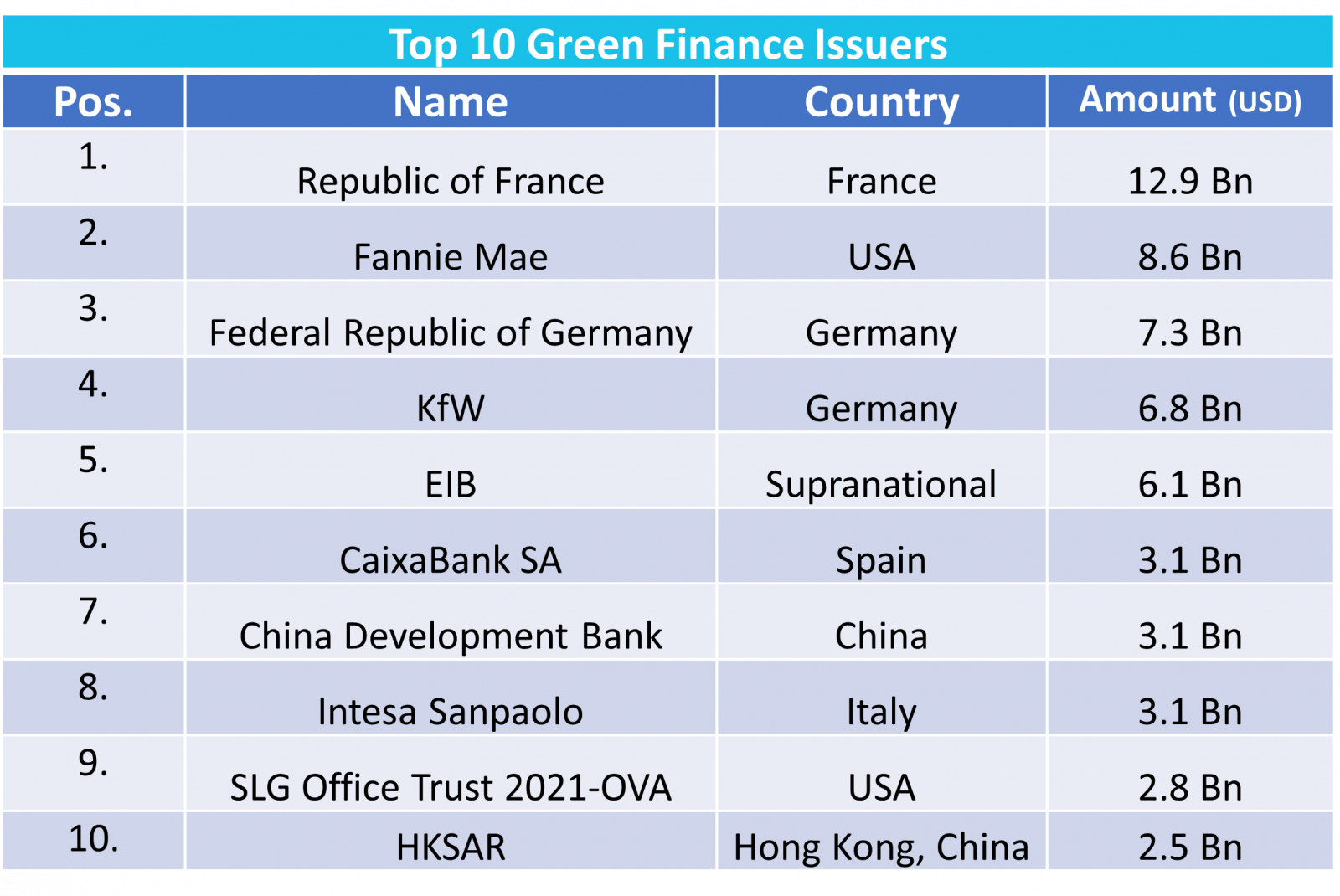

Sovereign Issuance Leads Green Market

The Republic of France was the top issuer, with three deals totalling USD12.9bn and making up over half of the segment’s issuance. Germany’s green Bund issuance followed in third at USD7.3bn in H1 2021.

Climate Bonds Certification

Certified Climate Bonds representing international best practice accounted for USD178 billion in volumes. Certifications were approved to 33 issuers from 18 countries.

The largest H1 Certified deal came from China Development Bank in March and amounted to approximately USD3.1bn. Other high-profile certifications included the latest from serial issuer Société du Grand Paris, who issued a USD2.4bn bond from April. The third largest in this category was the USD1.8bn covered bond from DNB, issued in January.

A recent USD80.6m Certification from Oberlin College puts them alongside Stanford University as major US educational institutions Certifying under the Climate Bonds Standard this year. Certifications also came from Japan Railway Construction, Transport and Technology Agency (JRTT), Azure Power – a leading independent renewable power producer in India, DNB Group – Norway's largest financial services group, and Faro Energy – a Brazilian solar energy firm, reflecting the huge reach of the Climate Bonds Standard.

At a Glance - Social and Sustainability bond issuance

Green bonds are classified in accordance with the Climate Bonds Taxonomy, while social and sustainability (S&S) bonds raise funds for projects with broader positive impacts across the spectrum of the Sustainable Development Goals (SDGs) and beyond specifically climate-related objectives.

S&S bonds comprised 47% of labelled debt issuance with USD233.3bn issued in H1 2021, up 18% year-on-year on the H1 2020 figure of USD197bn.

The result brings total cumulative S&S issuance since 2006 to USD867bn.

Bonds issued under the Social theme saw the sharpest increase, as their volume quadrupled in H1 2020 versus H1 2020 from USD36.8bn to USD146.6bn. Sustainability bond issuance also recorded 20% of year-on-year growth. Social bonds related specifically to funding COVID-19 mitigation and/or recovery were not issued in the first half of this year, while in the first half of 2020 they amounted to USD88bn.

At a Glance - Sustainability-linked bonds

Sustainability-linked Bonds (SLB) are forward-looking, performance-based debt instruments issued with specific Key Performance Indicators (KPIs) and Sustainability Performance Targets (SPTs) at the level of an entire entity.

The first half of 2021 saw the SLB market segment soar: SLB issuance in H1 2021 amounted to USD32.9bn, representing 6% of total labelled debt issuance of USD496.1bn for the six months. In contrast, no SLB issuance was recorded in the equivalent period of H1 2020.

At a Glance - Transition bonds

Transition bonds are designed to allow high emitters to fund their shift towards cleaner, more sustainable operations and strategies. When thoughtfully constructed, these debt instruments can be pivotal in supporting a global, economy-wide transition to the Paris Agreement targets.

The transition labelled bond segment remains nascent. Climate Bonds identified five transition bonds (USD2.2bn) issued in the first half of the year, and a cumulative total of 18 (USD6.4bn) since market inception.

The most prolific corporate issuer was Italian energy infrastructure company Snam, whose dual-tranche bond issued for a total of EUR750m (USD909m). The proceeds of the deal will be used to fund emission reductions, renewable energy, energy efficiency, green construction projects and the retrofit of gas transmission network to make it ready for lower-emission alternatives, including hydrogen.

Pressure on policymakers set to speed up green growth

In the UK, the Bank of England announced a change to its mandate to include environmental sustainability and net-zero transition. Its bond-buying program is set to include green bonds by the end of the year to keep with UK’s environmental pledges. The European counterpart ECB is taking integration of climate risk a step further by seeking to add a dedicated climate scientist to its team.

The EU Taxonomy Delegated Act and updated People’s Bank of China Green Projects Catalogue were released on the same day in April 2021, signalling increased international coordination to address climate change.

In the US, the change in administration has brought about increasingly positive signals including via the Biden Summit that the President hosted in April. The country has since made progress on a firmer climate target, and towards integrating sustainability considerations into its financial regulatory framework, including through the SEC.

Krista Tukiainen, Head of Research and Reporting, Climate Bonds Initiative:

"We are pleased that our initial projections for green bond market growth are likely to be exceeded, as other thematic issuance proliferates across a range of sustainability and SDGs related-outcomes. Climate Bonds will continue to monitor the global GSS market and the development of the transition label.”

“We expect a stream of COP26 timed commitments from the financial sector, more sovereign green issuance and an acceleration of policy measures, including the EU bond program, will all drive market growth towards a record 2021 and strong start in the first half of 2022.”

Sean Kidney, CEO, Climate Bonds Initiative:

“The green finance revolution is underway with a powerful beginning to a pivotal decade for climate action. These figures show the tremendous potential for acceleration in the market for this and following years. Reaching the vital milestone of the first $1trillion in annual green investment opens a green window in global capex flows against 2030 targets. Trillions towards clean technologies, transition and building climate resilience can become a reality. The climate emergency demands no less from policy makers, regulators and institutional investors.”

Coming Up - Expansion of Certification - Grids and Transition Certifications

As the market grows, Climate Bonds is continuing its expansion of sectors for Certification and the industry reach of the best practice Climate Bonds Standard. Desalination and Agri Livestock Criteria came to market in H1. Rollout of new Grids and Electical Storage Criteria is pending. (You can watch the Grids Webinar replay here). Even more exciting is our extension of Certification into transition finance, at the entity level, with a focus on heavy industry sectors, in particualr in the EU.

There's more information here and look out for the launch of our new 'Transition Finance for Transforming Companies' paper to be launched on Friday 10th September, Transition Day at a special session during Climate Bonds annual conference. Register here.

The Last Word

Climate Bonds original forecast of USD400-450bn in green bonds and several hundred in social and sustainability bonds has been overtaken by events.

At the halfway mark, the market is on track with USD227.8bn green at end of H1 and USD233.3 of social and sustainability bonds. We’re happy to have undershot on our initial assessments.

The Transition label is yet to reach the heights of the other labels but over the coming years, this too could play a prominent role. With Certitfication under the Climate Bonds Standard to become progessively available in 2022, the Transition finance market will have a new best practice foundation to build on.

Look for our full Q3 report for the next pointer to where 2021 will end up and what 2022 may hold.

'Till next time!

Climate Bonds