Curbing climate change and market development key motivations for sovereign green, social, and sustainability (GSS) bond issuance: First of its kind analysis: Sovereign GSS bond issuers

Climate action a priority for GSS issuers

Sovereign Green, Social, and Sustainability (GSS) bonds contribute to strategic government initiatives surrounding climate, catalysing local green finance markets and attracting new investors. These and other findings are contained in a comprehensive first of its kind survey undertaken by Climate Bonds.

Sponsored by HSBC, the ‘Sovereign Green, Social, and Sustainability Bond Survey’ was carried out during late 2020 to aggregate and assess the experiences of Sovereign GSS bond issuers and their role in market growth.

First-hand insights

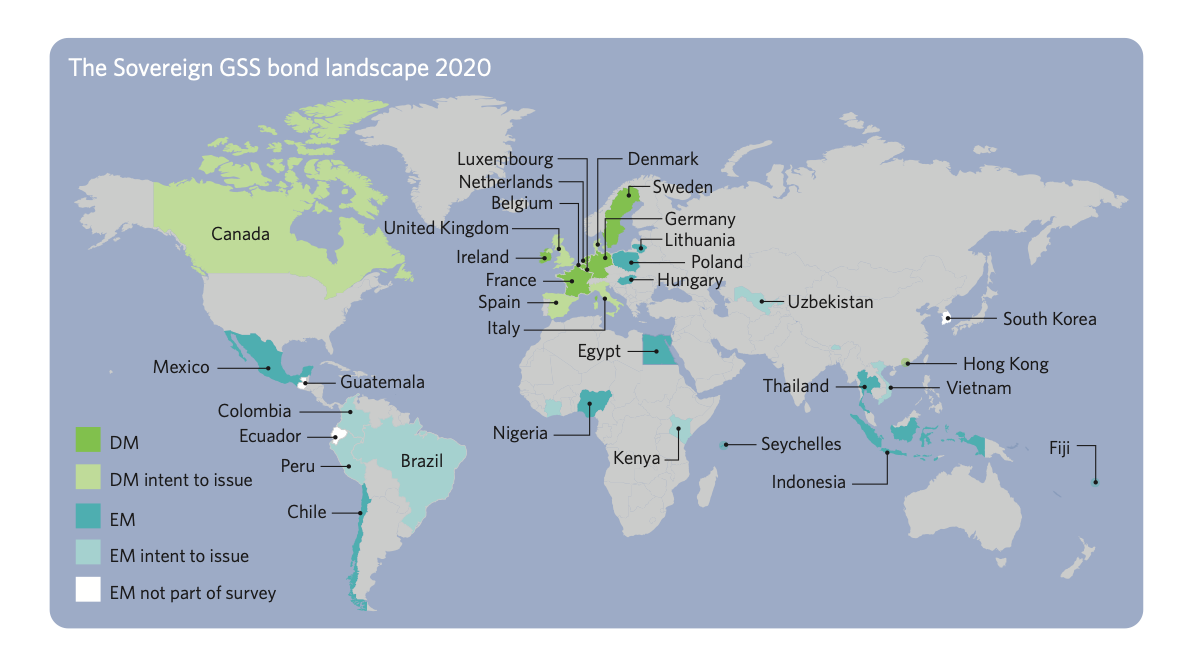

As of November 2020, twenty-two (22) national governments had issued sovereign GSS bonds totalling USD96bn. Nineteen (19) of the twenty-two bond issuers were interviewed for the Survey, comprising thirty-two GSS bonds with an amount outstanding of just over USD93bn. This sample covers a 97% share of the total sovereign GSS issuance.

Eight respondents were from Developed Markets (DM) and eleven were from Emerging Markets (EM). The survey explored in detail the full process of issuing a GSS bond and solicited views on additionality, as well as advice for other issuers.

Findings will be discussed in our Launch Webinar on the 28th of January 2021, 12.00 CET.

Supporting climate strategies, a trigger to issuance

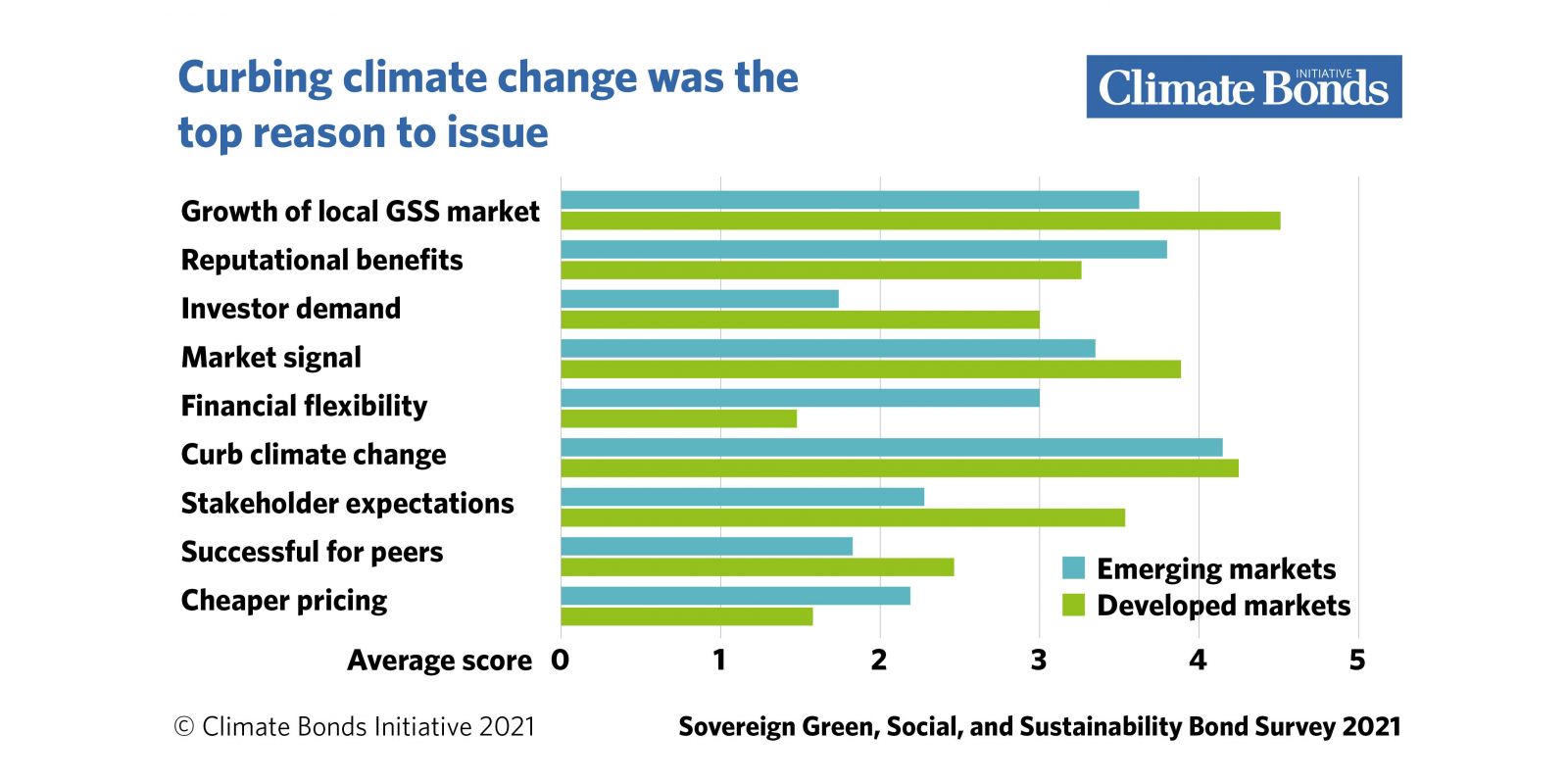

In most cases, wider strategic initiatives to achieve NDC targets, address SDGs, and mitigate climate change and social inequalities triggered the decision to issue GSS sovereigns. These plans included policies designed to address emission reduction goals as well as net-zero ambitions. With an average score of 4.2 (out of 5), curbing climate change was the leading reason why governments issue GSS bonds.

GSS played Catalyst role in market creation, collaboration and transparency

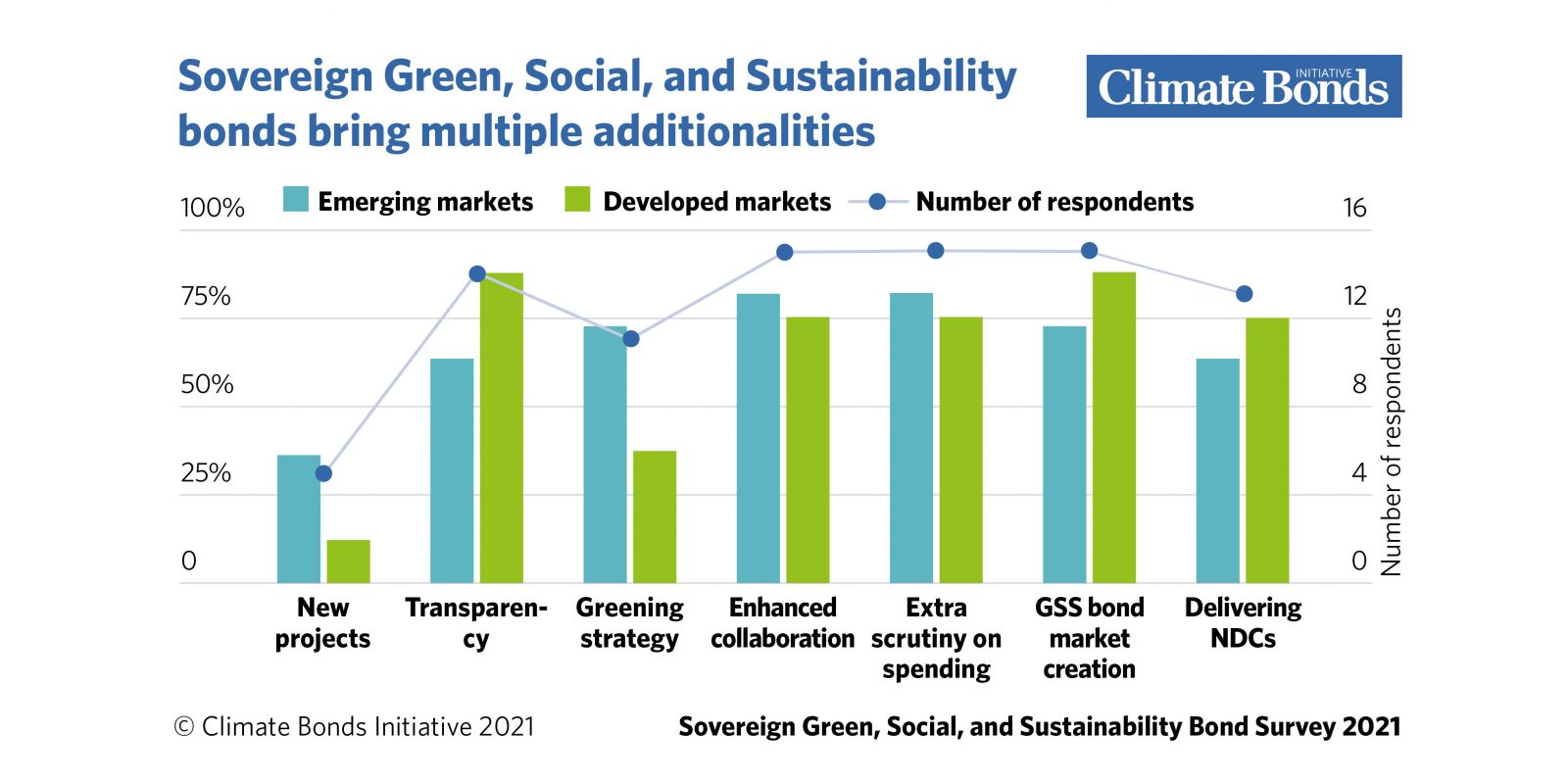

GSS bond market creation, as well as enhanced collaboration and extra transparency, were all considered additionalities by most participants. The former was stated as a key motivation for issuing a sovereign GSS bond by multiple respondents.

Sovereign issuers can be exemplary to other types of issuers and can provide investors with safe, liquid investment opportunities. As the process of issuing a sovereign GSS bond typically involved a budget tagging exercise and commitments to report on the allocation of proceeds and their impact, these audits greatly increase transparency for ministries, legislatures and extend to external stakeholders such as investors.

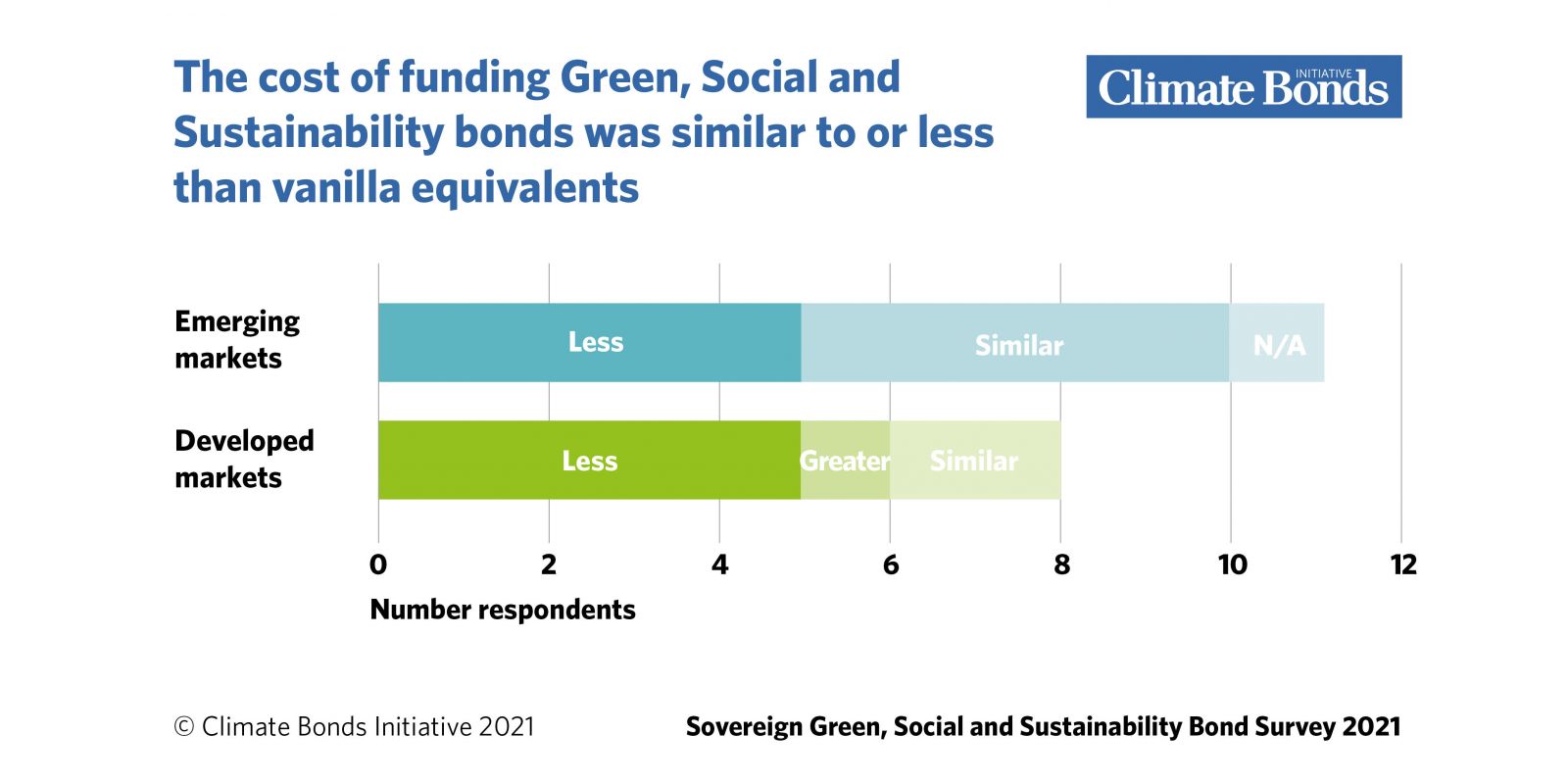

GSS bonds attract new investors: Offer pricing benefits

Most governments (79%) noted that a sovereign GSS bond broadened and diversified their investor base, a key motivation for issuing. A broader investor base can facilitate tighter pricing, and sovereign GSS bonds also encourage investors to initiate dedicated GSS investment strategies.

Robustness and reporting

Issuers advise and obtain a clear mandate from government, design a robust and simple framework, designate specific high-profile projects, and implement budgetary reporting standards. Issuers should not underestimate the commitment of post-issuance reporting and make sure they are well prepared.

Other highlights:

Facilitating cross border collaboration and enhance visibility.

Many respondents collaborated with Debt Management Office (DMO) counterparts both pre-and post-issuance, in knowledge forums and bilateral conversations. Even the Use of Proceeds (UoP) bore an element of international collaboration through funds being used to finance projects beyond the borders of the issuing country.

Governments can issue GSS bonds in less than a year.

Despite longer periods to get the ‘green light’ for issuing a GSS bond, once the decision has been made, 89% of the participants stated it takes one year or less to issue the bond.

Roadshows for sovereign GSS bonds differ from the usual setup.

Many participants stated – especially Developed Market issuers – that investors had a greater depth of questions and the team also extended to colleagues from other ministries.

National policies dictated eligible use of proceeds.

Most governments align their eligible expenditures to national policies. Other guides such as the ICMA Green Bond Principles are used frequently.

Jonathan Drew, Managing Director, ESG Solutions, Global Banking, HSBC:

“In a world now focused on the transition to a low carbon economy, sovereign green issuance is pivotal in funding the green investments to be made by the public sector and supporting the development of green finance markets. There is no doubt that sovereign green issuance has been key in raising awareness of the urgent need to tackle the climate crisis and the commitment of governments to take action.

“Public sector issuance has, by setting benchmarks and driving the creation of market infrastructure, been a catalyst in encouraging private corporate and institutional issuers to follow suit, and the mainstreaming of green considerations in financial markets.”

“With our international network, HSBC is well-positioned to provide support to sovereign green issuance across all regions. We are committed to bringing together public and private sector issuers with investors to drive the transition to a sustainable future.”

Sean Kidney, CEO, Climate Bonds Initiative:

“Sovereign green issuance sends a powerful signal of intent around climate action and sustainable development to governments and regulators. It catalyses domestic market development and provides impetus to institutional investors. “

“Multiple issuances even more so. Doubling the number of sovereign GSS issuers to forty (40) and supporting initial emerging market transactions should be amongst the immediate climate finance objectives for governments, central banks and development finance institutions.”

The Sovereign Green Bonds Club – How Big Could It Be?

In our December 2020 Blog post, Thai Govt Marks 2020 with Certified Sovereign Green Issuance: Commitment to Recovery, Sustainability, Infrastructure we identified an additional 14 nations that had foreshadowed inaugural green issuance in 2021-2022.

With President-Elect Biden now enjoying a razor-thin margin in the US Senate, the pre-Christmas speculation around the prospect of a green US Treasury bond will no doubt continue. Meanwhile, the EU program with its green and social components looms closer in 2021.

Prospects look a little brighter and there’s still plenty of room in the clubhouse for new members from G20, OECD, EU, ASEAN & MENA nations.

The Survey results speak for themselves on the benefits of sovereign GSS issuance around climate goals, green finance development, and with sufficient political impetus, the ability of sovereigns to come to market in a relatively short space of time.

Doubling the current number of Sovereign GSS issuers is the next milestone. We’ll mark progress towards the end of the year around COP 26.

'Till next time

Climate Bonds

The full report can be downloaded here.

And don’t forget the Report Launch Webinar on the 28th of January!

11:00 London / 12:00 Paris / 13:00 Cairo

Acknowledgements: Climate Bonds Initiative thanks HSBC for their sponsorship and support in the production of this report. We would also like to thank all our Survey participants for their time, cooperation and positive input.

Suggested citation: Harrison, C., and Muething, L., Sovereign Green, Social, and Sustainability Bond Survey, Climate Bonds Initiative, January 2021

Survey Background: Climate Bonds surveyed 19 sovereign GSS bond issuers speaking to individuals involved in the issuance process to gain a comprehensive understanding of the experience, benefits and challenges for governments to issue such bonds.

The survey captures sovereign green and sustainability bond issuers. They range from recent and one-off issuers to experienced issuers who joined the market in its early stages.

Respondents were divided into Developed and Emerging Markets. These categories are used to describe respondents throughout this paper.

Survey Participants:

Public Debt Department, Ministerstwo Finansow, Republic of Poland

Agence France Tresor, Ministere de l’Economie et des finances, French Republic

Belgian Debt Agency, Kingdom of Belgium Ministry of Economy,

Republic of Fiji Department of Blue Economy,

Republic of Seychelles Debt Management Office,

Federal Republic of Nigeria Ministry of Finance,

Republic of Indonesia EM DM

Ministerio de Hacienda (Hacienda), Republic of Chile State Treasury Department,

Ministry of Finance of the Republic of Lithuania

National Treasury Management Agency, Republic of Ireland

Hong Kong Monetary Authority, Hong Kong SAR

Dutch State Treasury,

Ministerie van Financien, The Kingdom of the Netherlands Government Debt Management Agency (ÁKK),

Republic of Hungary

Secretaria di Hacienda Y Credito Publico (SHCP), United Mexican States Debt Management Office,

The Kingdom of Thailand Ministry of Finance,

Kingdom of Sweden Deutsche Finanzagentur, Federal Republic of Germany Ministere des Finances, Grand Duchy of Luxembourg Capital Markets and Debt Management Unit,

Ministry of Finance,

Arab Republic of Egypt