Welcome to our latest English/Chinese newsletter for H1 2019

Highlights

-

2019 first half issuance from China at USD21.8bn/CNY143.9bn;

-

85% of all Chinese issuance was issued domestically. Singapore Stock Exchange was the most popular offshore listing venue;

-

Transport was the largest issuing sector;

-

Financial corporates remained the largest issuer type contributing 41% of total issuance;

-

A CNY1bn (USD14.9m) deal from Jiangsu Financial Leasing was the first Certified Climate Bond issued in China’s onshore market;

-

New Notice from the PBoC on supporting green financial reform and innovation pilot zones to launch green debt financing tools;

-

Full versions of the report in both English & Chinese can be found here.

Overview

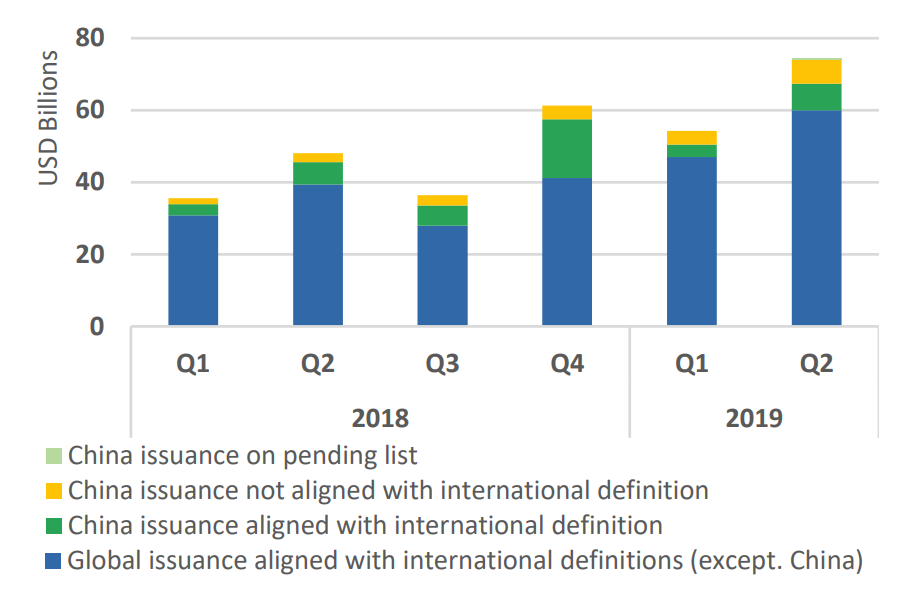

In the first half of 2019, total green bond issuance from China went up to USD21.8bn, a 62% increase year on year, largely due to contributions from regional banks and the private sector as a whole.

However, only 49% (or USD10.7bn) of H1 volume from Chinese issuers is in line with international green bond definitions. Another 49% has been excluded in accordance with CBI Green Bond Database Methodology. Of the remainder there are 5 deals on the Pending list, and they account for 2% (USD395.3m) of H1 issuance, where proceeds allocation disclosure is insufficient for us to determine alignment.

Issuance from financial corporates accounts for 41% of the H1 total issuance, followed by non-financial corporates at 34%, government-backed entities at 12.3% and ABS at 12.5%.

Use of Proceeds

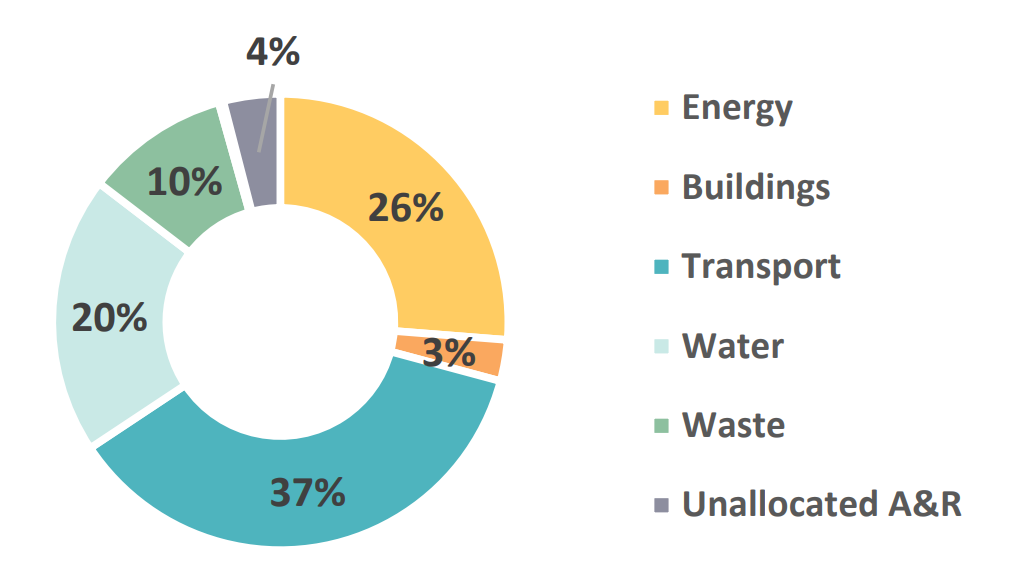

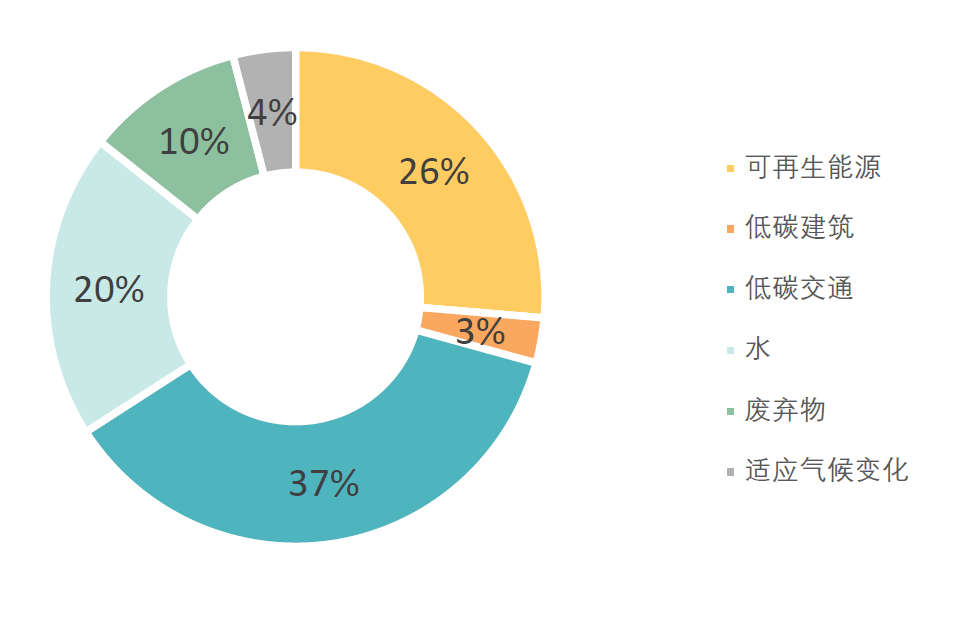

In terms of use of proceeds allocation, Low Carbon Transport has been the largest climate sector representing 37% of the total issued volume in H1 2019, followed by Renewable Energy (26%) and Water (20%).

Exclusions

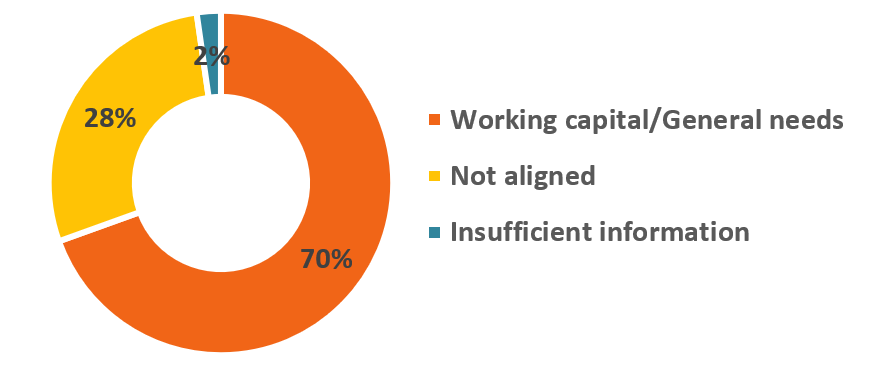

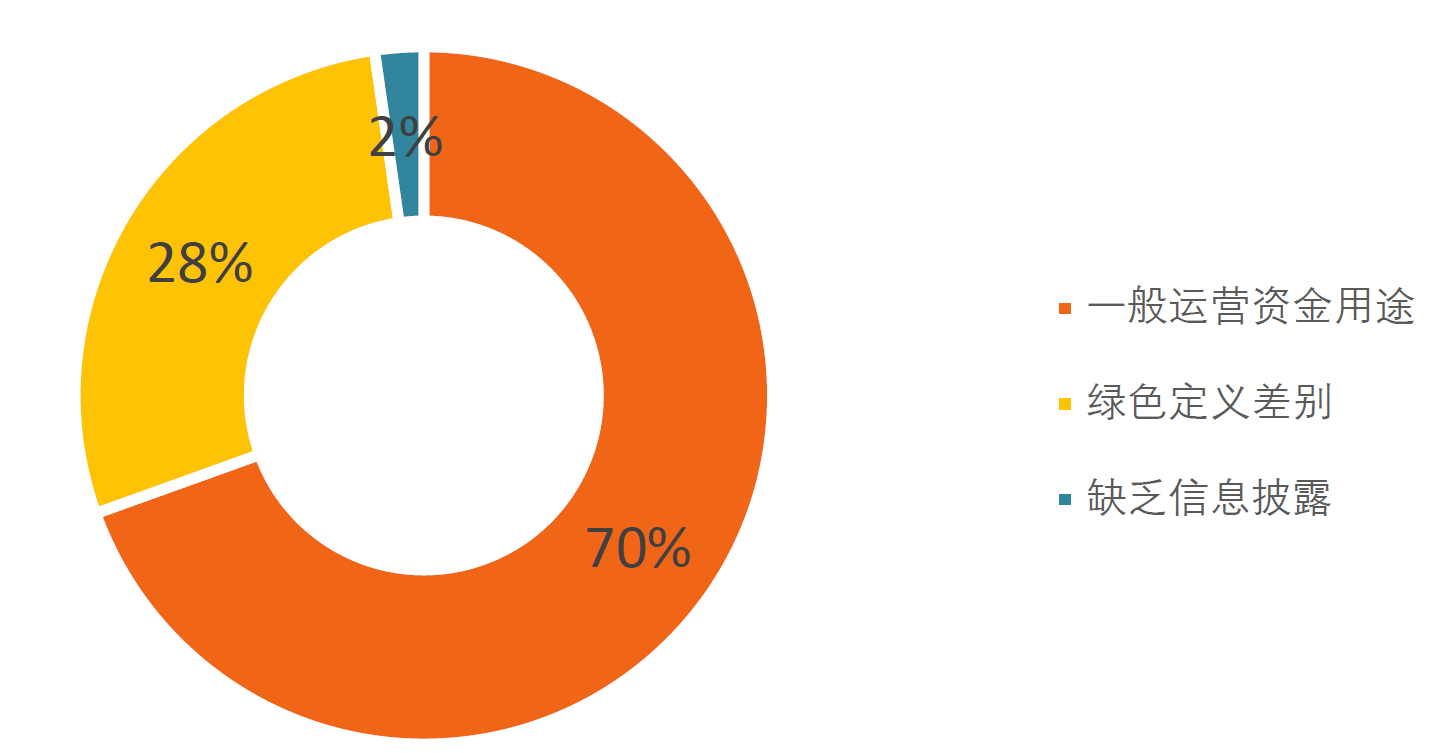

By amount issued, 70% of the overall excluded bonds in H1 fail to meet best practice as they allocate more than 5% of proceeds to general corporate purposes, not necessarily linked to green assets or projects. 28% of the excluded bonds are not aligned with international green bond definitions and the rest 2% fail to provide sufficient information.

The extras

In this latest report we also give a summary on how financial leasing companies in China are increasingly using green bonds as means for financing green assets, especially in the Energy, Transport and the Waste and Water sector.

Moreover, we’ve included local policy updates where assessment standards and implementation plans have been introduced to provide guidance on green projects eligibility and innovation pilot zones for carbon reduction, as well as pioneering measures in promoting green finance.

Read the full report here.

We hope you’ll enjoy it!

'Till next time,

Climate Bonds Initiative

中国绿色债券市场2019半年报:了解绿色债券发行人的最新动态和市场趋势,以及全球第二大绿色债券市场的发展情况

亮点:

-

2019年上半年来自中国的绿色债券发行量为1439亿人民币/ 218亿美元

-

85%的中国发行为在岸发行。同时,新加坡证券交易所是最受欢迎的离岸挂牌地点

-

低碳交通为最大的募集资金投向领域

-

江苏金融租赁的10亿元人民币(1.49亿美元)绿色债券是首只在中国境内发行的认证气候债券

-

中国人民银行:支持绿色金融改革创新试验区发行绿色债务融资工具

点击此处下载本报告中英文的完整版本。

概览

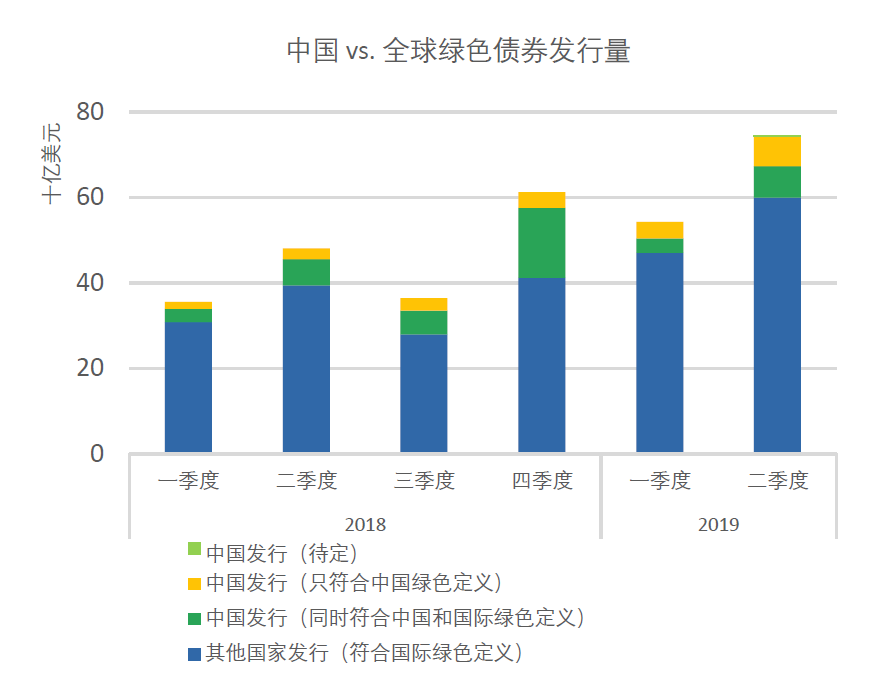

2019年上半年,中国发行的绿色债券总额达到1439亿人民币(218亿美元),同比增长62%,这主要由银行和企业的发行而驱动。然而,来自中国的发行只有49%(718亿人民币/107亿美元)符合国际绿色债券定义,根据CBI绿色债券数据库方法论,另外49%被排除在外。有5只债券处于待定状态,占发行总额的2%。待定原因是募集资金分配的信息暂不足以支持判断。

金融企业发行量占2019年上半年发行量的41%,其次是非金融企业,占34%,政府支持机构占12.5%,ABS占12.5%。

募集资金用途

在募集资金的分配方面,低碳交通为最大的募集资金用途类别,占2019年上半年总发行量的37%。其次是可再生能源(26%)和水(20%)

不合符国际定义的绿色债券

将募集资金投向一般用途的运营资金仍然是不符合国际定义的主要原因。上半年不符合CBI定义债券总额的70%是因为将超过5%的募集资金用于一般运营资金,且这些运营资金并不一定与绿色资产/项目相关。28%是因为支持与国际绿色债券定义不一致的项目或资产,其余2%未能提供足够的信息以支持判断。

在本报告中,我们还概述了中国的金融租赁公司如何越来越多地使用绿色债券作为绿色资产融资的手段,特别是在可再生能源、低碳运输、废弃物和废水处理领域。

此外,我们还纳入了地方政策更新,包括关于地方绿色项目资格评估标准、减碳试验区实施方案,以及促进绿色金融的开创性措施。

点击此处下载英文和中文季报

祝阅读愉快!

气候债券倡议组织