The first half of 2017 has seen public sector issuance, regulator moves, and new market incentives to energizing domestic green bond markets.

Download our analysis of 2017 1st and 2nd Quarter’s biggest green bond policy developments. We look back on the last six months and look ahead to developments for the remainder of the year.

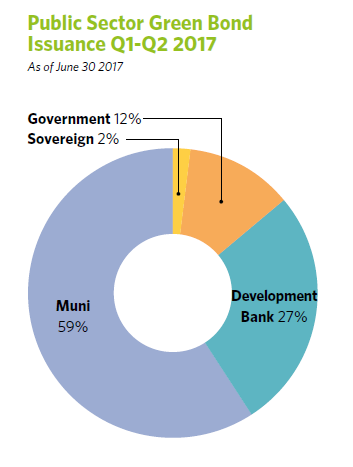

Six Months into the year of sovereign green bonds

Our 2016 end of year policy roundup pointed to 2017 as the year of the sovereign green bond. France delivered their first sovereign green bond in January and amongst emerging economies Nigeria is expected to come to market later this year.

We are looking at between 8-10 nations to have issued or signaled an intention to issue by the end of the year.

Beyond sovereigns, Canada, Australia and Argentina have also set great examples of how provinces and states can get the ball rolling on green bond issuance. Sub-nationals and sub-sovereigns may yet steal the limelight if national leaders are slow to act.

We also saw a debut issuance for $587 million by the National Bank of Abu Dhabi, an exciting first for the Gulf region. More national banks need to do the same.

Regulators release new guidelines

Several nations have made progress in developing green bond guidelines and ensuring the process for domestic green bond issuance follows international best practice.

- The China Securities Regulatory Commission issued guidelines broadly aligned with PBoC’s green definitions, with minor provisions.

- India’s Securities and Exchange Board (SEBI) has finalised its guidelines for domestic issuers

- Japan, Luxembourg and Taiwan are making strides and other intiatives are underway in South Africa, Nigeria, Indonesian and through ASEAN.

Central banks announcing green bond incentives

The Monetary Authority of Singapore has launched a Green Bond Grant Scheme to support issuers with the cost of external reviews - a burden which is often brought up by issuers who are yet to approach the market.

PBoC in China is exploring the possibility of allowing green bonds in the bank’s collateral framework as well as the integration of green lending in macro-prudential assessment frameworks.

We hope to see more actions from central banks in the near future given their crucial role in addressing financial stability, including risks associated with climate change.

U.S. green bond growth

The U.S. green bond market can still expect to see significant growth, despite President Trump’s decision to withdraw from the Paris Climate Accord.

Overwhelmingly, key actors at the state, city investor, and at corporate level have reiterated support for the Paris Accord and reaffirmed their climate pledges. At a subnational level, California is leading the way in growing domestic climate finance and green bond markets with an extensive action plan.

The Last Word

Total green bond issuance for the year currently sits over USD$53 billion, and with favorable circumstances we now hope to see that number reach USD$130bn by the end of the year, down a little from our Jan/Feb forecast.

Public sector policy is essential to enabling and scaling up private capital flows into green bond issuance and investment at a rapid rate. The EU HLEG Sustainable Finance process is an example.

$1Trillion by 2020?

We’re also heartened to see global climate leaders call for green bonds to be scaled up tenfold by 2020, one of six urgent climate action milestones they identify.

That would give a glonal market size of around $1trillion, a level of climate finance that would significantly boost progress on NDCs and implementation of country climate plans.

What a platform that would make for the critical COP 27 in 2021!

Governments at all levels have well-established tools that have been previously used to steer private capital towards policy priority areas. They can again be applied to enable green markets and channel capital towards climate firendly infrastructure and investment.

This is the public policy challenge. We have the tools, we have the timeline and we have the targets.

Let’s see what progress we can report on by years end.

Download the Q1-Q2 Update here.

‘Till next time,

Climate Bonds

PS: We are looking for a Climate Science Programme Manager. It's an exciting job, based here in London. Details are here.

Disclaimer: The information contained in this communication does not constitute investment advice in any form and the Climate Bonds Initiative is not an investment adviser. Any reference to a financial organisation or debt instrument or investment product is for information purposes only. Links to external websites are for information purposes only. The Climate Bonds Initiative accepts no responsibility for content on external websites.

The Climate Bonds Initiative is not endorsing, recommending or advising on the financial merits or otherwise of any debt instrument or investment product and no information within this communication should be taken as such, nor should any information in this communication be relied upon in making any investment decision.

Certification under the Climate Bond Standard only reflects the climate attributes of the use of proceeds of a designated debt instrument. It does not reflect the credit worthiness of the designated debt instrument, nor its compliance with national or international laws.

A decision to invest in anything is solely yours. The Climate Bonds Initiative accepts no liability of any kind, for any investment an individual or organisation makes, nor for any investment made by third parties on behalf of an individual or organisation, based in whole or in part on any information contained within this, or any other Climate Bonds Initiative public communication.