It’s all about clean green infrastructure!

Last week Lord Stern, author of the seminal review from way back in 2006, gave a 10 years on from the Stern Review anniversary address at the London School of Economics, followed the next day by an address to the Royal Society titled Stern Review +10: new opportunities for growth and development.

Here at Climate Bonds, some of us made it to the LSE session and we’ve reviewed both the videos and presentations.

Here’s our favourite takeaway:

“Infrastructure is central to the growth story”

“Expected future emissions from existing power plants alone will take us over 2C with 50% probability”

“For Paris and Sustainable Development Goals (SDGs) to succeed, global infrastructure investment must nearly all be clean/green from now on”

“Infrastructure investment is central to Paris COP21, SDGs and spurring global growth”

The respective PowerPoints’ and audio/video pages from LSE here and Royal Society here.

We can’t recommend them highly enough.

Corporates

Certified Climate Bond from France’s SNCF EUR 900m – Bravo!

France’s rail operator SNCF has just announced its first Certified Climate Bond.

The bond has been certified by the Climate Bonds Standards Board with a verification provided by Oekom.

The proceeds will be allocated to investments related to heavy maintenance and upgrade of the rail system, as well as new rail lines and rail extension.

The bond has a 15-year tenor, which is above average for the green bond market. The bond was oversubscribed with order books reaching EUR 1.35bn.

Underwriters: HSBC, JP Morgan, Credit Agricole

More SNCF green bonds to come

The rail operator already has an extensive bond program, dominating the figures for climate aligned issuance in our recent France Overview, released in September.

As part of this announcement, SNCF has signalled they will to issue further benchmark green bonds on an annual basis.

You can read more here in English or French.

Allez allez!

Hong Kong’s MTR Green bond USD 600m – a funding model for others to follow!

Last week MTR, Hong Kong’s rail network operator, issued its first green bond (USD 600m, ten-year tenor).

Proceeds for the bond will finance quite an extensive list of sustainability based projects:

- Low carbon transportation (metro rail, rail and light rail)

- Energy efficiency in rail construction and operation (e.g. systems and timing optimisation, new energy efficient trains and buses)

- Energy efficiency in property management (lighting, HVAC, etc.)

- Sustainable stations (LEED/BREEAM certified buildings)

- Climate adaptation (upgrades to systems to adapt to extreme weather events e.g. flood protection)

- Biodiversity and conservation (reforestation, ecological restoration, soil remediation)

- Water management (rainwater collection, water efficiency technologies)

- Waste management (recycling, separation of materials to increase recycling)

- Pollution prevention (air filtration, noise reduction)

There is a lot in there - it all looks good - subject to some further information about level of ambition when it comes to buildings - but we expect much of the proceeds will be concentrated on the rail upgrades, improvements and efficiencies, given the nature of their business.

Sustainalytics provided the review of the Green Bond Framework.

The bond was priced at the tight end of the range, following strong demand from a diverse group of institutional investors and green investors in Hong Kong, Asia and Europe.

Underwriters: Bank of America Merrill Lynch, Goldman Sachs, HSBC.

Value capture and new infrastructure

We must admit - we are pretty excited about this one – mostly because it gives us an opportunity to wax lyrical about the ingenious nature of MTR’s funding model.

So here we go…

If transport improvements are made providing a new area with access to public transit (e.g. new rail line or station) – this gives an immediate boost to adjacent land and property values (through no action of the landholder) which is a positive externality of the new project.

A ‘value capture’ model allows for this boost in value to be captured and then used to repay for metro, bus rapid transit or rail development.

Value capture can be done in several ways including tax increment financing districts, development charges, development rights, and joint development.

How MTR does value capture

MTR’s model is basically the holy grail of transport networks – it’s big (5 million people per day), efficient (99.9% on schedule), reasonably-priced and profitable – yes you heard right: profitable.

They do all this through a value capture model to recoup the cost of infrastructure investments which they call ‘rail plus property’.

In the case of MTR, the Hong Kong SAR, China, government gives exclusive property development rights of government-owned land at stations or depots along the route to MTR Corporation.

MTR pays the government a land premium based on the land’s market value without the railway.

MTR then builds the new rail line and partners with private developers to build properties above and around the stations. MTR then leases or sells the land at the incremented value. This generates finance for more rail and public finance projects. Given that they are self-sustaining, they also do not have to compete for public funds which means more rail projects are built more quickly.

Ingenious.

Want to know more? See quite a good explanation here.

Chinese property developer Modern Land issues USD 350m green bond

Modern Land became the first mainland Chinese property developer to issue green bonds last week with a 3-year USD 350m bond.

Proceeds will finance projects that have a high likelihood of obtaining green building certification and achieve additional energy saving targets of 15 percent for new construction and 30 percent for renovations.

Details are scarce at this stage, CICERO reviewed the framework which is a positive but unfortunately the documentation is not public yet.

Underwriters: Guotai Junan, Morgan Stanley, HSBC, UBS, VTB Capital and Zhongtai International.

Vasakronan issue latest green bond for SEK 400m (USD 45m)

Back to Sweden with another green property bond. Vasakronan might not be the biggest issuer but they are important as; a) one of the first issuers of corporate green bonds (way back in 2013) and b) one of the most regular issuers.

Proceeds of Vasakronan green bonds are used to finance construction and renovation projects that achieve LEED Gold (or higher).

The following links will take you to the Green bond Framework, review from: CICERO and their reporting on previously issued bonds.

Underwriters: Danske Bank and Svenska Handelsbanken.

Datang Renewables RMB 500m (USD 74m)

Beijing based China Datang Corporation Renewables Power Co Ltd (Dating Renewables) have issued their 2nd green bond in just over a month.

It’s an easy one folks - all proceeds will be used for four wind farm projects, including one offshore wind farm (300MW capacity) and three onshore wind farms (700MW capacity in total).

Hard to get much greener than that, but to sweeten the deal, they have also put together an excellent disclosure of the environmental impact of each project.

For example, they state that the offshore wind farm will deliver 791GWh a year, which equivalent to saving:

- 260K tons of coal

- reducing 660K tons of CO2

- 4,746 tons of SO2

- 1,899 tons of NO2

Great stuff!

The 14th September and 21st September notices to the Hong Kong Stock Exchange are here and here.

Review from EY.

Underwriters: Credit Suisse Founder, Huatai United

Wuhan Metro RMB 2bn (USD 414m)

China’s Wuhan Metro is the latest rail issuer to join the market with a RMB 2bn green bond to finance low carbon transport development.

The proceeds will be distributed as follows: RMB 1bn to develop three metro lines; RMB 1bn to refinance four metro lines.

Wuhan is the capital city of the province of Hubei in Central China, with a population of over 10 million.

The Wuhan metro system only started operating in 2004 (becoming the 5th Chinese city to have a metro system) and yet, amazingly, it now carries 1 – 1.5 million passengers per day!

It has 128km of track (London Underground has about 400km) and very ambitious plans for expansion!

Review: China Credit Rating Co., Ltd.

Underwriters: China Development Bank

China’s State Grid Corp issues RMB 10bn (USD 1.5bn) green bond for transmission lines

Chinese state owned enterprise (SOE) State Grid Corp, has just issued its first green bond for RMB 10bn. State Grid builds and operates the power grid across China.

Half of the proceeds will finance the construction of four high-voltage transmission lines from Western China in the nation’s Eastern regions, while the other half will be used for the company’s daily operation.

The disclosure specifically states that one of the projects is connecting a wind farm to the grid. The remaining projects are unclear.

Transmission lines are an essential part of renewable energy transmission and are eligible for green bond financing in the PBOC green definitions.

Grid infrastructure has been part of previous green bonds internationally. For example, Dutch grid operator TenneT has issued several successful green bonds in the last 12 months to finance transmission lines to connect offshore wind farms.

However, to meet international expectations of green, there needs to be a clear link that new grid infrastructure is being built to connect renewable energy. While this is clear for one of the lines included in this bond, for the remaining three lines and the 50% of proceeds that are going to general corporate purposes, the link is unclear.

We will therefore leave this one off our list for the moment but note that the part of the bond that is financing the grid to connect renewables does qualify, so hopefully they will do plenty more like that in the future!

Underwriters: China Galaxy, China Merchant Securities, CITIC, Everbright, Shenwan Hongyuan Securities, Yingda Securities

Poten Environment Group issues RMB 300m (USD 44m)

Beijing based water and eco-environmental services company Poten Environment has issued a new green bond, with proceeds intended to finance the construction and operation or repay bank loans for four sewage plants. It is listed on the Shanghai Stock Exchange.

Sewage is a tricky area and we have recently released enhanced criteria for Grey Infrastructure Assets. The release of these criteria will allow investors to prioritise which types of sewage plants, treatment and technologies are in line with a low carbon economy.

This is particularly important as we are seeing more bonds, particularly out of the US municipal market, which are financing water, sewage and wastewater projects.

Adaptation planning is clearly an important component to any green project, but there are other factors too – so watch this space!

In their news release, Poten are pointing to this issuance as the first corporate green bond issued by a non-listed privately owned company in China.

External review: EY

Underwriters: China Securities, Western Securities

Municipal Bonds

Kommuninvest smashes green bond SEK record with SEK 5bn deal

In our last blog, we spoke about the ingenious Nordic municipality debt aggregators that support sustainable housing.

Well, here is a green bond from another one. Kommuninvest priced its second green bond for the year for SEK 5bn and in so doing, it smashes the record for SEK-denominated green bond deals (previous highest was SEK 2.5bn).

The book was over 5 times oversubscribed at over SEK 13billion. Investors included: Alecta, AP3, AP7, Danske Capital, Folksam Group, Nordea Asset Management, KfW, SBAB, SPP Storebrand and Öhman.

The bond will finance lending to Swedish municipal investment projects in:

- renewable energy

- energy efficiency

- green buildings

- public transport

- water management

Kommuninvest is a regular green bond issuer and has built up a green loan book amounting to SEK 14.5bn (USD 1.6bn), committing funds to some 60 projects in 40 Swedish municipalities, councils and regions.

Renewable energy and green buildings account for the clear majority of projects in the portfolio, at 43 percent and 39 percent, respectively.

Underwriters: SEB, Swedbank

Norway’s Kommunalbanken issues USD 500m green bond - Another Nordic aggregator

Last market blog it was the Nordic property issuers, this blog it’s the muni aggregators! After a bit of a break, Kommunalbanken have issued their first bond of the year, their 7th issuance overall.

Eligible green projects include:

- renewable energy

- low carbon buildings

- waste and wastewater management

- sustainable land use

- low carbon transport

- climate adaptation

To date, the lending portfolio has been diverse, with most of the spending going into low carbon transport (46%), green buildings (22%) and waste/wastewater management (27%). See more here.

CICERO provided the review.

Underwriters: Citi, Credit Agricole, SEB

Aloha! – First Green Bond from the City of Honolulu out soon for USD 143.6m

The City and County of Honolulu has sold its first ever green bond. The proceeds will be used to refinance debt which was originally sold to pay for the Honolulu Program of Waste Energy Recovery (H-POWER) in Kapolei.

H-Power is a waste-to-energy plant processing about 600,000 tons of waste annually and producing approximately 10% of Oahu’s energy (60,000 homes). Waste management is not the glamourous end of the spectrum but this 2 minute clip from Oahu is worth a quick look.

The city said this week the green bonds were well received, with more than USD 475m in orders from investors (including dedicated green investment funds) that had never purchased Honolulu bonds.

Long term Market Blog readers will recall previous solar issuance from Hawaii in 2014 and again for habitat preservation in 2015.

Hana hou** to Hawaii!

Lead underwriter: Bank of America Merrill Lynch

(** “Encore/do it again” in Hawaiian)

City of Napa USD 12.5m green bond for waste management facilities

The Californian city of Napa in the heart of the Golden State’s wine making territory has made its first foray in the green bond market with a USD 12.5m green bond to finance upgrades to its materials diversion facility, which processes a wide range of recyclable materials.

About USD 7m of the funding will pay for a new process for breaking down organic wastes (in which finished compost will cover fresh waste to improve air quality) and a roof will shield the facility to lessen storm water contamination.

The bond issue will also include a USD 2.5m upgrade of the storm water collection and treatment system, as well as the USD1m roof extension to cover the composting complex and limit runoff.

The prospectus is here.

Underwriter: Raymond James & Associates, Inc.

Connecticut green bond USD 65m

US state of Connecticut has carved out a USD 65m green portion of its USD 650m bond issued this week.

The green portion will finance various high priority clean water projects across the State for design, construction and improvements to wastewater treatment plants and related energy efficiency upgrades; designed to reduce water pollution according to State and federal standards.

Other important investments include projects designed to improve water quality in the State’s rivers and Long Island Sound by separating storm water from sanitary sewer systems in urban areas.

Prospectus is available here.

Underwriter: Wells Fargo

Iowa Finance Authority issues USD 163.3m green bond

The bond will finance projects that bring communities in line with the Clean Water Act and Safe Drinking Water Act. This includes the improvement of water pollution control and sewage facilities.

Prospectus here.

Private Placements

YES Bank places INR 3.3bn green bond (USD 49.7m) with Dutch investor FMO

YES Bank placed a INR 3.3bn green bond with Dutch investor (and green bond issuer) FMO. The proceeds will be used to finance green infrastructure including solar and wind projects.

Great news - Bravo FMO and Yes Bank!

We are proud to note that FMO is a partner of the Climate Bonds Initiative.

Gossip

City of Tamarac, Florida prices first green deal (closing 09/11/16) - here.

City of Cape Town announces plans to issue a Certified Climate Bond in 2017.

LA Sanitation District about to issue Green Bond for USD 170m (closing 16/11/2016) see here.

Dongjiang Environmental plans to issue RMB 1bn green bonds.

Tokyo Metropolitan Government to issue soon their inaugural!

India’s IDBI have put out their Green Bond Framework. No bond yet but the framework received a review from KPMG.

Tokyo is planning to issue AUD 10bn ‘Tokyo Environment Supporter Bonds’. Marketing will start in November and the bonds will be sold mainly to Japanese retail investors. Use of proceeds is for solar PV, greenery for public parks etc. More here in Japanese.

Sweden joins the race for the first sovereign green bond!

Green bonds make it into the Goa Declaration for the BRICS.

Green bonds repackaged for retail investors in Australia.

Mexico City plans to issue MXN 1bn of green bonds to finance public transport, water efficiency and wastewater management.

Nigeria sets Quarter 1/2017 target for sovereign green bond issuance.

Kenya's green bond policy to be in place in early 2017.

Italian sovereign green bond rumours? The Ministry of Public Debt says "it's a novelty to be investigated, but not immediately".

Green Bond guidelines coming out of Japan? The Japanese Ministry of the Environment published a release which says an “investigative commission for green bond” will be held to establish Green Bond Guidelines.

UK energy supplier Ecotricity launches 4th Ecobond.

California green bond issuances top USD 1bn mark.

IFC issued inaugural forest bonds.

Latvenergo gets Moody’s GB assessment.

Rhode Island issues Green Economy bond.

Destiny USA's tax-exempt 'green bonds' violated the law, ex-IRS official says.

French Banking Federation (FBF) calls for lower capital requirements for green loans - the proposed policy called the Green Supporting Factor (GSF), aims to "recognise the macro-prudential benefits of green assets in reducing the probability of climatic risks."

FBF has modelled the GSF on a pre-existing EU policy that requires banks to hold 76% of the normal capital requirements when lending to small and medium-sized enterprises (SME).

Reuters is reporting China’s Bank of Communications has gained regulatory approval to issue up to RMB 30bn (USD 4.5bn) in green bonds. Announcement in Chinese here.

Brazilian development bank BNDES, already a major investor in renewables is cutting lending for fossil fuel energy and increasing investments in clean power. More here.

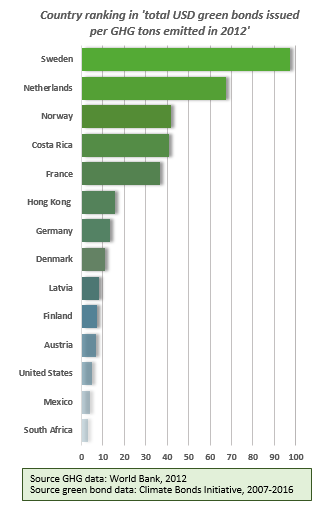

Quirky graph of the week

Nordic countries appear to have the highest ‘green bond issuance per GHG tons emitted’ ratio.

You’ve made it all the way to the end of the Blog!

As a thank you, here’s the link to the full version of Leo DiCaprio’s new documentary film on climate change 'Before the Flood', now available on YouTube.

Till next time,

The Markets Team

Disclaimer: The information contained in this communication does not constitute investment advice and the Climate Bonds Initiative is not an investment adviser. Links to external websites are for information purposes only. The Climate Bonds Initiative accepts no responsibility for content on external websites.

The Climate Bonds Initiative is not advising on the merits or otherwise of any investment. A decision to invest in anything is solely yours. The Climate Bonds Initiative accepts no liability of any kind for investments any individual or organisation makes, nor for investments made by third parties on behalf of an individual or organisation.