16 June 2021

Media Release – Invitation to report launch

ASEAN SUSTAINABLE DEBT MARKET HITS RECORD ISSUANCE VOLUME IN 2021

New report by Climate Bonds and HSBC presents latest numbers and key trends to be followed to strengthen sustainable finance in ASEAN

Register now for the webinar launch on Friday 17th June.

The sustainable debt market in the 6 largest ASEAN economies continued to grow rapidly in 2021 with record issuance of green, social, and sustainability (GSS) debt totaling USD24bn compared to USD13.6bn in 2020, up 76.5% YOY, and sustainability-linked debt totaling USD27.5bn compared to USD8.6bn in 2020, up 220% YOY.

This growth reflects the regions’ enthusiasm to allocate capital for the response to the COVID-19 pandemic along with facilitating long-term, low carbon, and climate-resilient economic growth.

Key highlights from the ASEAN sustainable debt market in 2021 include the following:

-

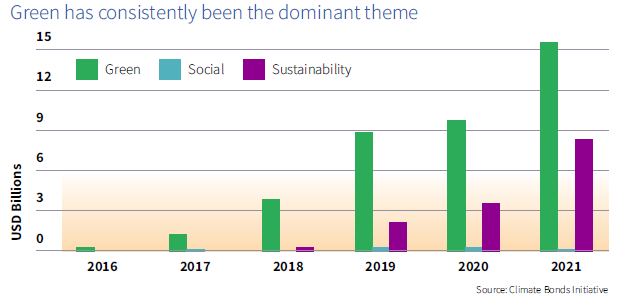

Green-labelled debt, encompassing green bonds and green loans, remained the most popular in the GSS debt market in 2021. 63.9% of GSS deals originating from ASEAN in 2021 were green, followed by sustainability (35.5%), with the latter showing an increase compared to 2020 (26%). The region saw a small volume of social debt issuances (0.6%) in 2021.

-

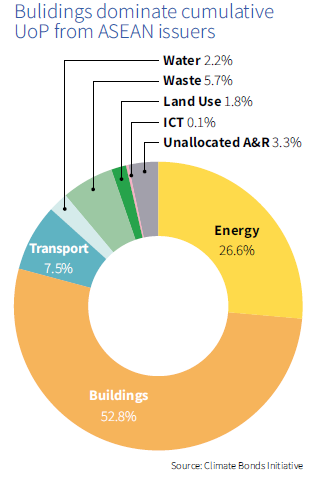

Buildings and Energy continued to represent the main use of proceeds for green-labelled debt in ASEAN. The two sectors received two-thirds of proceeds in 2019 growing to 79% in 2020. The cumulative regional picture remained the same in 2021. Buildings and Energy combined accounted for 79.5% of the cumulative use of proceeds of green debt issued from the ASEAN region between 2016-2021.

-

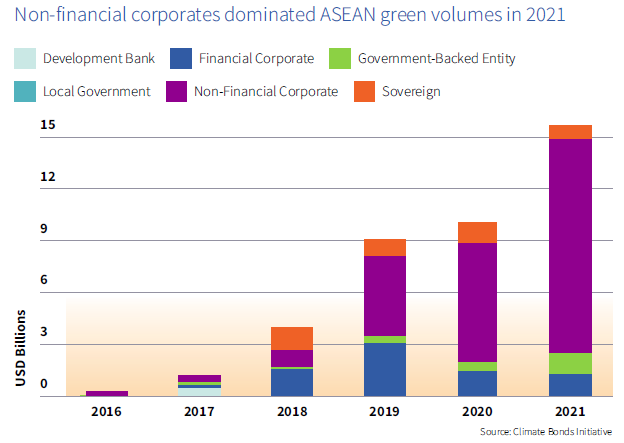

Non-financial corporate issuers were responsible for most (79%) of the ASEAN green volumes in 2021, while sovereign issuance continued to dominate the social and sustainability market, responsible for 51% of issuances.

-

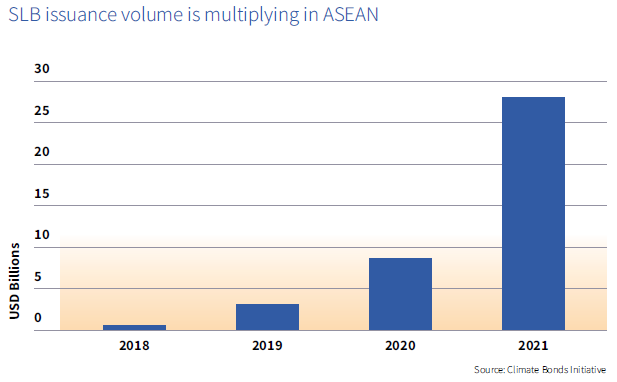

Sustainability-linked debt saw an exponential growth, adding USD27.5bn of sustainability-linked bonds (SLB) and sustainability-linked loans (SLL) in 2021 and thereby exceeding the traditional GSS debt volumes. The cumulative figure for the SLL and SLB markets at the end of 2021 was similar to that of the green-labelled debt at around USD39bn.

-

The transition bond market is still nascent. ASEAN saw its maiden transition bond in 2021 with the Chinese Construction Bank in Singapore issuing a USD2bn deal designed to support China’s carbon-intensive industries, such as gas and other power generators, manufacturing, and steel production.

Growth in the ASEAN sustainable debt market continued to be encouraged by supportive regulatory developments in 2021. Work has been underway to establish green taxonomies that will provide a clear and common definition of sustainable activities. At the regional level, the ASEAN Taxonomy Board released a draft ASEAN Taxonomy in November 2021, while an increasing number of countries are progressing in developing their own taxonomies, such as Malaysia, Singapore, Thailand and Vietnam. Government grant schemes to subsidise the cost of GSS bond issuers has remained available, such as in Singapore and Malaysia. Requirements regarding sustainability reporting for corporates have been strengthened, as seen in Singapore, Indonesia and Thailand.

Investor demand is also growing from multiple sources. This includes greater understanding of climate risk from investors as well as enthusiasm to explicitly align sustainable investments with the UN Sustainable Development Goals and Paris agreement goals.

Kelvin Tan, Managing Director, Head of Sustainable Finance & Investments, ASEAN, HSBC said:

“We are encouraged by the significant growth in sustainable debt issuance across ASEAN in 2021. While this growth is partly driven by enhanced regulatory support, there is an increasing trend where more companies are aligning climate risk with their business strategies. In particular, this has led to a notable increase in interest from corporates in sustainability-linked loans, which provide the flexible use of proceeds while still enabling corporates to achieve their sustainability objectives and targets. However, significantly more financing needs to be deployed, to mitigate and adapt to climate change. This mobilization of finance will support our transition into a low carbon economy, which will be critical to achieve the Paris agreement goals and mitigate the devastating effects of climate change for the ASEAN region.”

Sean Kidney, CEO, Climate Bonds Initiative said:

“Several regional policies contributed to a rapid growth in sustainable finance in ASEAN and it’s clear there’s greater understanding of climate risk from both policy makers and investors. Despite the enthusiasm we see in the market, there’s still a huge gap that needs to be addressed - and quickly. High-emission and hard-to-abate sectors must transition from brown-to-green rapidly. That includes activities, assets and projects linked to energy, heavy manufacturing industries and agriculture. Local initiatives such as the Green Financial Industry Taskforce of Singapore (GFIT) are a good start, but we need to move quicker to make vulnerable regions like ASEAN less exposed to the consequences of climate change.”

Country Highlights

Country-level updates focusing on notable deals, policies and initiatives are also unpacked in the report.

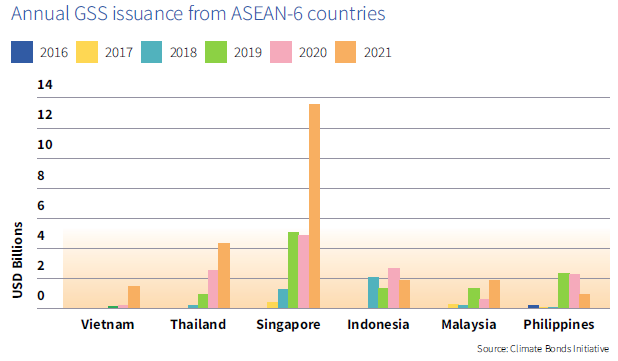

Singapore, Thailand, Malaysia, and Vietnam saw an increased volume of GSS debt issuances compared to 2020, while Indonesia and the Philippines saw a decline following strong issuances in 2020.

Singapore

Singapore remained the regional leader, with GSS debt issuance of USD13.6bn in 2021 compared to USD4.9bn in 2020. The growth is mainly driven by the green theme and reflects strong support for green finance from the Singaporean government. In ASEAN, Singapore was the largest source of green debt with volume of USD12bn. Together with Indonesia, Singapore has the most diverse mixture of deal sizes, ranging from below USD100m to above USD1bn. Singapore was the largest source of ASEAN sustainability-linked loans and bonds at the end of 2021, with 94 out of a total of 129 deals with a cumulative volume of USD33.6bn, accounting for 84.5% of the market.

Thailand

Thailand is the largest source of sustainability debt, with cumulative volume at USD 5.8bn by the end of 2021, or 38% of the cumulative ASEAN social and sustainability market. The majority of green bond issuances in 2021 continued to come from transport and energy.

Thailand emerged as the regional leader in social and sustainability issuances in 2021. The 2020 sovereign sustainability bond issued to finance green transport and social impact projects to assist with COVID-19 recovery- was reopened seven times, amounting to USD3.04bn in 2021. This led to a remarkable increase in the issuance volumes of the social and sustainability label in Thailand in 2021, totaling USD3.6bn.

Indonesia

Among the ASEAN-6 countries, together with Singapore, Indonesia has seen the most diverse mixture of deal sizes, ranging from below USD100m to above USD1bn. In September 2021, Indonesia was the first country to issue a sovereign SDG bond in Southeast Asia, raising USD 584m to fund social and environmental projects to support SDGs. At the end of 2021, the Indonesian GSS+ market was dominated by the green theme, but with growing shares of sustainability and sustainability-linked instruments. Green debt leads the Indonesian market at 65% of volume followed by equal shares of sustainability bonds and sustainability-linked instruments at 15% each. Social bonds make up a 5% market share.

Malaysia

Malaysia saw three consecutive years of growth in the GSS+ market. The sustainability label remained the most prominent financing instrument, accounting for roughly half (51%) of the cumulative market share. Green debt (bonds and loans) accounted for 29% of the market, followed by 20% from sustainability-linked instruments. In April 2021, the Government of Malaysia issued the world’s first sovereign USD-denominated sustainability sukuk, a USD800m 10-year deal. The proceeds will be used for eligible green and social projects aligned with UN SDGs

Vietnam

Vietnam had a GSS volume of USD1.5bn in 2021, almost five times the USD0.3bn in 2020 and maintaining steady growth for the third consecutive year. Major green bonds and loans in Vietnam in 2021 came from the transport and energy sectors. Vietnam was the second largest source of green debt in ASEAN in 2021 at USD1bn.

The Philippines

The Philippines also saw slowdown in 2021, with USD0.9bn of GSS debt compared to USD2.3bn in 2020. The country saw two green bond issuances in 2021 from the energy sector. Green debt originating from the Philippines is mostly in the medium-sized category (USD100-500m), but also extends to smaller (up to USD100m) and larger (USD500m- USD1bn) deals. UoP debt makes up 93% of the GSS+ volumes in the Philippines market, split 52% of green and 41% of sustainability debt. Sustainability-linked instruments accounted for 7% of the cumulative volume at the end of 2021.

The full report is available for download on Climate Bonds website and HSBC Centre of Sustainable Finance website.

For more information, please contact:

Head of Regional Communications, Climate Bonds Initiative

+55 (61) 98135 1800 (Whatsapp)

Lucy Stewart

Senior Communications Manager, HSBC

+65 93892611

Notes for journalists:

About the Climate Bonds Initiative: Climate Bonds Initiative (Climate Bonds) is an international organisation working to mobilise global capital for climate action. It promotes investment in projects and assets needed for a rapid transition to a low-carbon, climate resilient, and fair economy. The mission focus is to help drive down the cost of capital for large-scale climate and infrastructure projects and to support governments seeking increased capital markets investment to meet climate and greenhouse gas (GHG) emission reduction goals. Climate Bonds conducts market analysis and policy research; undertakes market development activities; advises governments and regulators; and administers a global green bond Standard and Certification scheme. Climate Bonds screens green finance instruments against its global Taxonomy to determine alignment, and shares information about the composition of this market with partners. The aim is to help build investment products that enable shifting capital allocations towards low-carbon assets and projects.

About the ASEAN SoTM series: This is the fourth iteration of the Climate Bonds Initiative’s ASEAN State of the Market Report series. As the sustainable debt market has grown, the scope of this report has expanded, and now includes analysis of the green, social, and sustainability (GSS) bond and loan markets, plus sustainability-linked bonds (SLBs) and sustainability-linked loans (SLLs) and transition bonds, collectively described as GSS+ debt. It also covers unlabelled bonds from climate-aligned issuers. This report describes the shape and size of GSS+ themed and unlabelled climate-aligned debt market originating from ASEAN and priced on or before 31 December 2021.

HSBC Holdings plc

HSBC Holdings plc, the parent company of HSBC, is headquartered in London. HSBC serves customers worldwide from offices in 64 countries and territories in its geographical regions: Europe, Asia, North America, Latin America, and Middle East and North Africa. With assets of $3,022bn at 31 March 2022, HSBC is one of the world’s largest banking and financial services organisations.

Disclaimer: The information contained in this communication does not constitute investment advice in any form and the Climate Bonds Initiative is not an investment adviser. Any reference to a financial organisation or debt instrument or investment product is for information purposes only. Links to external websites are for information purposes only. The Climate Bonds Initiative accepts no responsibility for content on external websites. The Climate Bonds Initiative is not endorsing, recommending or advising on the financial merits or otherwise of any debt instrument or investment product and no information within this communication should be taken as such, nor should any information in this communication be relied upon in making any investment decision. Certification under the Climate Bond Standard only reflects the climate attributes of the use of proceeds of a designated debt instrument. It does not reflect the credit worthiness of the designated debt instrument, nor its compliance with national or international laws. A decision to invest in anything is solely yours. The Climate Bonds Initiative accepts no liability of any kind, for any investment an individual or organisation makes, nor for any investment made by third parties on behalf of an individual or organisation, based in whole or in part on any information contained within this, or any other Climate Bonds Initiative public communication.