Central banks in the hot seat on systemic sustainability

The powerful toolkit of the central bank, lying beyond the often-lethargic legislative process, is increasingly being recognised as a key agent in affecting climate action. And this action is swiftly needed. As COP26 looms ever closer, the Climate Bonds Policy Team outlines what they hope may come from central bank attendees.

Exceeding Expectations

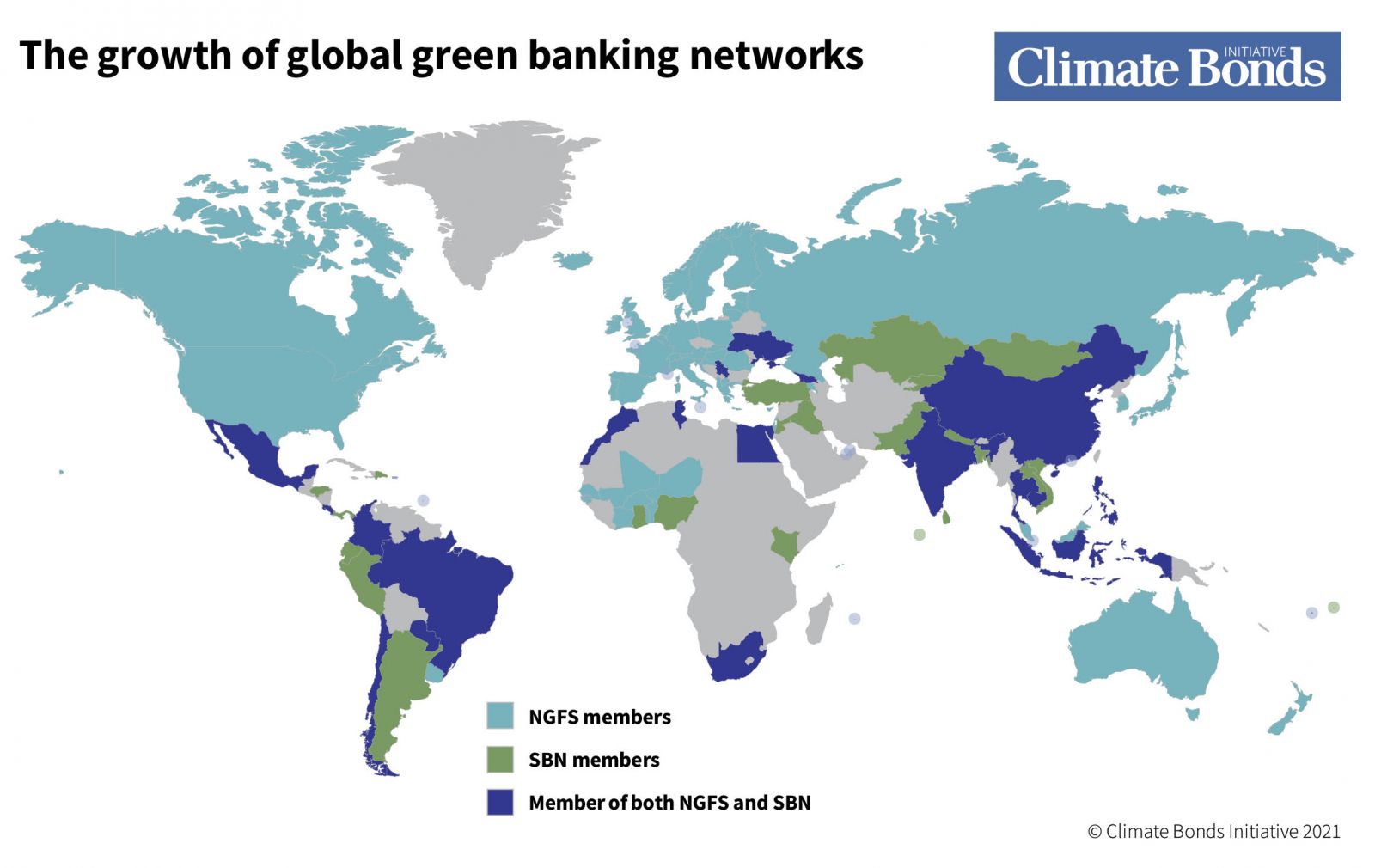

Established in 2017, the Network for Greening the Financial System (NGFS) unites members in a mission to enact environment‑related risk management and mobilise finance to support a sustainable economic transition. Climate action by central banks has since accelerated in a way that has exceeded many expectations.

Its membership has swollen from 8 to 95 as of June 2021 with the December 2020 addition of the US Federal Reserve addressing a vital gap. This growth in participation reflects both the increasing prioritisation of green finance by central banks and supervisors, but also the value of knowledge-sharing and collaboration when navigating these still reasonably uncharted waters.

The below map of NGFS and Sustainable Banking Network members illustrates that central banks across the globe are acknowledging the materiality of climate change to financial stability; several members have since implemented climate risk disclosure or stress testing requirements.

Building Back Better

In the last year, we have seen unprecedented action at all levels of central bank functioning, from prudential adjustments to green monetary policy strategies, to actual mandate changes.

The COVID-19 pandemic demonstrated central banks’ powerful role in a crisis. The crisis response illustrated the capacity of central banks to increase resilience and target economic sectors most in need. At the same time, recovering from the pandemic has been posited as an opportunity to ‘build back better’.

In May, our Primer suggested that measures seen in the pandemic, such as increased risk tolerance in collateral frameworks, or standing facilities targeting small and medium-sized enterprises (SMEs) could be repurposed towards a green recovery.

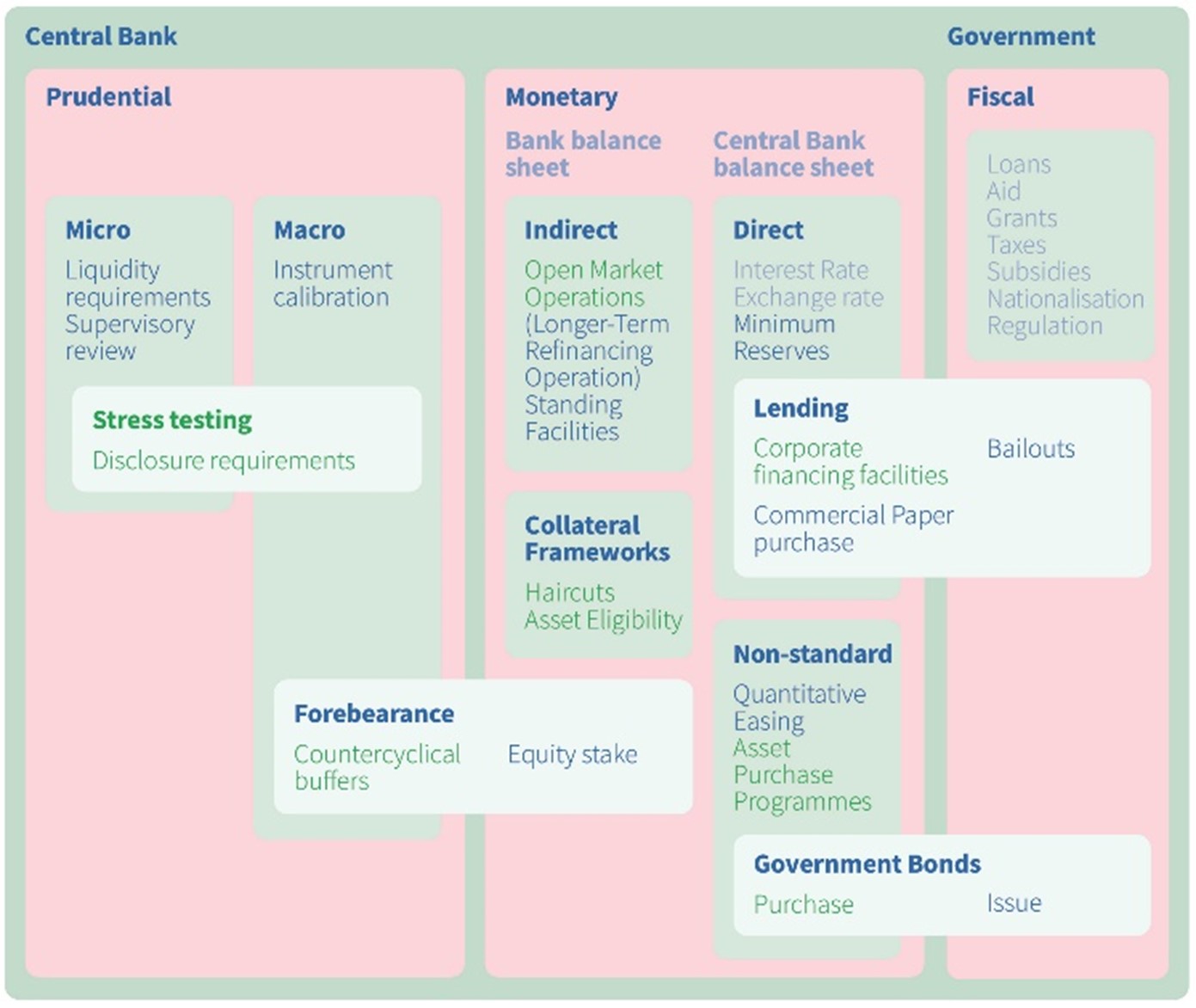

Opportunities lie in every element of the central bank’s toolkit

However, significant work remains to be done if central bank operations are to truly set economies on a path to net zero. In 2019, our Tilting the Playing Field report outlined key monetary and prudential policies that could stimulate green investment, and as we have outlined in a recent report, almost all aspects of central bank operations can be greened:

Climate change necessitates that central banks forego the luxury of waiting several years for the results of economy-wide disclosure or stress test regimes. The IPCC’s Sixth Assessment Report confirms this decade to be our last chance to avoid catastrophic climate breakdown. There is evidence enough on which companies are most exposed to, or are the largest sources of, climate-related risk.

This was emphasised in the Bank of Japan’s recent announcement of a new “fund provisioning measure” for green finance, of zero-interest loans for banks investing in green projects, which came with the statement by Governor Haruhiko Kuroda that “it is not appropriate for us or other central banks to wait around [for international agreement on green taxonomies]”.

A death knell for climate neutrality?

Market neutrality is the principle that the central bank should not unduly influence the market and so purchase corporate bonds in the same proportions as the market. However, when asset purchases reach EUR3 trillion and markets are oversaturated with carbon-intensive companies, such action cannot be seen as neutral.

Market neutrality limits the extent to which monetary operations can be greened, as the high capex and longevity of fossil fuel companies leads them to dominate the market. NGFS modelling has proven that significantly shifting portfolio emissions requires more than just boosting green bond purchases, fossil exposures must also be severely limited.

The nature of climate change is such that in all areas of government and the economy the need for, and reliance on, forward-looking scenarios and metrics is clear. This makes the principle of market neutrality one which seems increasingly outdated.

There is hope given by the ECB’s market neutrality review. Prominent figures at the ECB such as Frank Elderson and Isabel Schnabel have argued for the end of market neutrality and President Christine Lagarde has questioned it. Proposals for alternative principles will come in 2022.

For those central banks with stress tests and disclosure requirements in place, replacing market neutrality with climate neutrality may be the next step, if they want to continue their trailblazing role and truly tilt their economies towards a decarbonisation pathway.

The IPR View

Climate forecasting group the Inevitable Policy Response (IPR), cites regulator fears of climate-based financial instability as one of the underlying forces that will accelerate climate policymaking to 2025. The latest NGFS scenarios analysing climate risks to the economy and financial system published in June reinforces this view in the broad ‘Orderly’, ‘Disorderly’ and ‘Hot House World’ scenario categorisations adopted.

IPR also sees extreme weather events and civil society pressures amongst other drivers exerting continued pressure on policymakers to take rapid action leading up to the 2025 Paris Stocktake. Reaction to the fires, floods and heatwaves of the first half of 2021 bears out this assessment, and the growing discussions at G20 Finance and Central Bank Governors summits around sustainability and stability are a signal that sharper decisions on global financial regulation will emerge in the immediate years ahead.

The extent to which central bank directions are included in the initial report of the reconstituted G20 Sustainable Finance Working Group (SFWG) due in October and the multi-year G20 Roadmap on sustainable finance, will provide some early indications.

COP26: The Next Chance for Change

It is imperative that central banks demonstrate commitment to climate action by implementing sustainability strategies. This will facilitate coordinated action across all areas of operation and provide clear direction to the market.

DNB, the Netherlands central bank has been a leader in climate-related risk analysis, and has recently launched its Sustainable Finance Strategy, which covers risk management, research and data and monetary operations. As we recently explored, the ECB’s new climate action plan promises alignment of monetary policy with the Paris Agreement, although the extent to which operations will tilt towards sustainable activities remains to be seen.

We hope that COP26 will see the launch of many more sustainability strategies by central banks.

The Last Word

“Fire, the wheel and central banking.” These are the three greatest inventions since the dawn of time, according to the American humourist Will Rogers. Central banks have been evolving in recent years and now wield considerable tools to influence markets. They now need to mobilise these tools not only to preserve their own economies’ stability but to ensure global resilience to potentially irreversible planetary changes.

Fired-up, wheels turning. The next stage in central banks’ evolution must address the relationship between economic activity and environmental degradation. This is where the role of global policymakers is critical as IPR notes.

Collectively, central banks and regulators can only go so far of their own volition. Governments, through the various climate, diplomatic and economic forums must provide continued green signals for change.

We’ll be looking to COP26 as one of those forums to provide a kick start to a new age of climate considerations in central banking.

Stay tuned for more Countdown to COP26 coverage from the Climate Bonds Policy Team!

Til’ next time

Climate Bonds

The KangaNews* Jun/Jul 2021 magazine is now available to read online.This edition includes Australia’s first SLB for transition, a take on adding sustainability to the inflation-linked bond

renaissance, coverage on SLLs flavour of the month in Australia and New Zealand and more.

Click here to view the magazine online or download a PDF.

If you are a magazine subscriber and are having trouble accessing the new magazine or would like to see more of KangaNews's online content, please contact Jeremy Masters.

*KangaNews is a media partner for Climate Bonds Conference21.