We’ll be discussing the results and conclusions during a Webinar scheduled for Wed, 27 November 2019, 11:30 – 12:30 GMT.

Why not join us? Register now here.

Forty-eight of the largest Europe-based fixed income managers participate in Climate Bonds first green bond investor survey

With supporting analysis from Henley Business School of Reading University and sponsored by Credit Suisse, Danske Bank, Luxembourg Stock Exchange and Lyxor Asset Management, the Green Bond European Investor Survey was undertaken during 2019 to identify approaches that would accelerate EU based and global green bond issuance.

We asked investors how they perceive the green bond market. The main aim was to explore the drivers, challenges and required tools and incentives which could encourage investors to buy (or buy more) green bonds and support market growth.

Key Findings:

Investors are looking for green transition opportunities: Corporate issuance was nominated by 93% of respondents as one of their preferred green bond investment channels followed by development banks at 76% and sovereigns on 57%. (See Sector Findings)

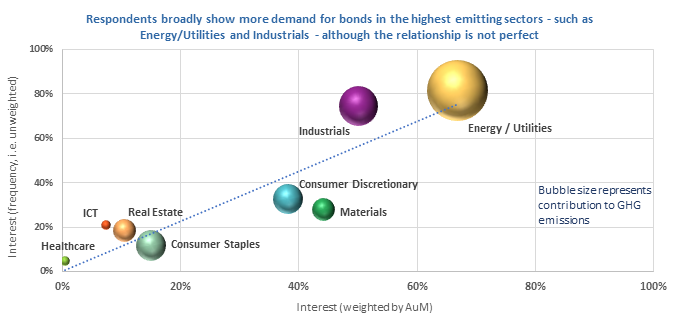

Investors want deals with high climate impact: The survey found a positive correlation between the level of interest in industry sectors with the pollution level (measured by GHG emissions) of those sectors. Respondents highlighted Industrials, Energy and Utilities, Consumer Discretionary, and Materials as the top sectors of interest. (See Sector Findings)

Investors highly value green credentials and transparency: All else being equal, the most important factor for making a green bond investment decision is satisfactory green credentials at issuance. Respondents demonstrated high expectations of integrity, with 79% saying they would definitely not buy a green bond if the proceeds were not clearly allocated to green projects at issuance, and 13% would be less likely to. On the flip side, 55% would definitely sell if post-issuance reporting was poor, and 30% would be more likely to.

Policy key driver to investment: Respondents view policy as the most effective way to scale up the green bond market, with standardisation of definitions being a priority. Policies such as tax incentives and differentiated capital treatment of low- versus high-carbon assets, designed to channel investment from high- to low-carbon assets, are also regarded as having high potential. The results also revealed a preference for tax incentives over subsidies within the investor community – at present, only Malaysia has developed tax incentives for green bond issuers and investors.

Lack of supply: There is strong investor appetite for green bonds, with respondents consistently expressing demand for more bonds from more issuers in more sectors. Almost two-thirds of respondents (64%) said they prefer green bonds where available and competitively priced (over vanilla equivalents); over half of these also have a specific green bond fund and/or mandate.

A deeper look

Corporates and sovereigns are the most demanded issuer types:

There seems to be a mismatch between investors’ preferences for different issuer types and their share of the green bond market. Corporates – both financial and non-financial – and sovereigns garnered the highest interest from respondents, with non-financial corporates and sovereigns ranking far above their position in the current green bond market. This points to opportunity particularly for these two issuer types to increase green bond issuance.

On the flip side, development banks and green securitized bonds were significantly less demanded compared to their current green bond market share. From an investor standpoint, and relative to other issuer types, perhaps this suggests development banks could more effectively support the market’s growth “indirectly” rather than as green bond issuers themselves, e.g. through de-risking tools (such as credit guarantees and insurance policies), anchor investing (for instance via private placements or junior debt), providing technical assistance, etc.

Spotlight on sectors

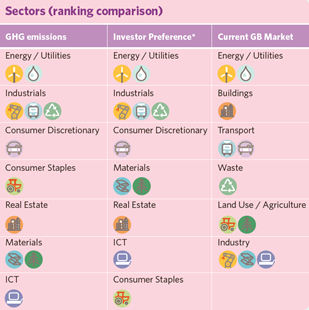

Corporates were identified as the most demanded issuer type. To delve into sectors, we asked respondents to list the top three non-financial corporate sectors in which they would most like to buy green bonds (according to GICS). The following emerged as the top five sectors, significantly above the rest:

- Industrials (e.g. transportation, machinery, services)

- Utilities (e.g. electric, gas, water)

- Consumer Discretionary (e.g. automotive, retail, electronics)

- Energy (e.g. oil & gas, but for renewable energy projects)

- Materials (e.g. metals & mining, chemicals, forestry products, construction materials)

We also compared the level of interest with each sector’s GHG emissions. There cannot be a perfect match between the two because the activities of some sectors lend themselves to debt financing better than others, and companies in those sectors are thus more able to issue green bonds, but the results are nonetheless interesting.

There is a broad positive correlation between the level of interest in sectors with their GHG emissions. This is likely due to the higher need for green investment being precisely in the most polluting sectors, and the fact that green bond issuance is severely lacking in some high-emission sectors like Industrials and Metals/Mining.

Even so, Materials – and to some extent Industrials – garnered relatively more interest from respondents than their emissions would suggest, whilst Consumer Staples (e.g. agriculture) seems to be less demanded relative to its level of pollution. It is also noteworthy that Consumer Discretionary is considerably more in demand than Consumer Staples, despite similar GHG emissions, due to substantial demand for automotive bond exposure.

Who's saying what?

Marisa Drew, CEO Impact Advisory and Finance Department, Credit Suisse:

“This survey is an important benchmark and source of high-quality feedback demonstrating how far the green bond market has evolved over the past decade. The size of AUM represented by the respondents and the increasing level of sophistication and rigour they are applying to the analysis of these instruments is a strong indicator of the support for, and adoption of, this market. It also reinforces the critical role the capital markets can play in helping the world allocate capital towards addressing climate change.”

“Investors also remind us in this survey, that improved transparency, standardisation, clear linkages of proceeds to green outcomes, and the inclusion of a wider issuer universe are all key to unleashing the full potential of green finance markets. This will require a concerted effort from issuers, underwriters, ratings agencies, regulators and policy makers.”

Bo Søndergaard, Head of SRI Bond Marketing, Danske Bank:

“The investor survey from Climate Bonds Initiative again provides us with some very useful information and offers some good insight to investor thinking, which in turn can help drive the green bond market even further. As an example, investors have been calling for increased transparency via allocation reporting and impact reporting, especially regarding greenhouse gasses, long identified as of high importance. This survey gives proof of those thoughts in a compiled format, strengthening our arguments in issuer advising discussions.”

“It is also encouraging to see investors expressing a strong interest for green corporate issuance, identified as the most in-demand issuer type.”

Julie Becker, Member of the Executive Committee of Luxembourg Stock Exchange and Founder of the Luxembourg Green Exchange:

“The survey highlights the unmet demand for green bonds, and clearly suggests that there is a lack of adequate supply, especially from corporate issuers. Respondents call for more diversification in green bond issuers, and we hope that such feedback from the investor community will lead to an uptick in green bond issuance from corporate players. If we are to reach the UN Sustainable Development Goals, the private sector needs to mobilise and help drive the transition into a low-carbon economy.”

François Millet, Head of ETF Strategy, ESG & Innovation at Lyxor AM:

“Lyxor has pioneered the green bond ETFs market, launching the world’s first ETF on green bonds and is committed to providing investment solutions to aid climate transition. After partnering with CBI last year to conduct the first-ever survey on the French green bond market, we are happy to be a part of this new survey which sheds light on how investors’ expectations are shaping up this fast-growing market in Europe.”

Sean Kidney, CEO, Climate Bonds Initiative:

“The survey tells us that investor demand for green is strong and continues to build. There's a particular interest in companies and industries transitioning to green.”

“Robust offerings from heavy emitting industry sectors and their underlying corporates that demonstrate a credible brown to green commitment, corporate transition and capex plans that align with Paris goals and a zero-carbon direction will attract continuing institutional investor support.”

"The opportunity for policy-makers and governments is to build on this momentum to achieve the rapid capital shift towards low carbon investment is needed. Regulatory support and fiscally efficient incentives and policy measures can be instrumental in accelerating the market.”

The Last Word:

These results point to a sophisticated investor base, with the knowledge and capital needed to address climate change issues through investment decisions.

Issuers, particularly those in sectors with the largest GHG emissions, can absorb this capital by issuing green bonds to fund their transition to a low carbon, climate resilient business model.

When asked about the key driver and barrier for green bond market growth, most respondents gave policy-related answers. This suggests policy is paramount to being able to scale up investment into green projects.

Finally, issuers and investors alike must play a role in driving greater transparency and better visibility to support the market. A green bond platform providing aggregated information, possibly even including standardised reporting by issuers, could be especially powerful.

The Green Bond European Investor Survey 2019 can be downloaded here.

We’ll be discussing the results and conclusions during a Webinar scheduled for Wed, 27 November 2019, 11:30 – 12:30 GMT. Register now here.

What’s next:

This is Climate Bonds Initiative’s first green bond investor survey in what is planned to become a series of surveys. The results of this survey will be complemented by our upcoming issuer survey, which will help to shed more light on these topics from the perspective of green bond issuers.

‘Till next time

Climate Bonds

Acknowledgements:

Climate Bonds Initiative thanks Credit Suisse, Danske Bank, Luxembourg Stock Exchange and Lyxor Asset Management for their sponsorship and support in the production of this report.