The latest in the series of “Green Bond Pricing in the Primary Market” reports

The 6th publication is now available which identifies H1 (Q1-Q2) 2018 as the first period in which green bonds have performed better than vanilla equivalents in both EUR and USD in terms of having larger book cover and greater spread compression. 17 out of 23 EUR green bonds, and 6 out of 6 USD bonds had larger oversubscription than vanilla equivalents.

This follows detailed analysis of the performance of 23 EUR and 6 USD denominated benchmark size green bonds with a total value of USD29.4bn issued during H1 (Q1-Q2) 2018.

This is the first semi-annual report, marking the period January - June 2018. Previously, the report was released on a quarterly basis, the first one being the Q4 2016 Snapshot.

Highlights from Q1-Q2 2018:

- 23 EUR and 6 USD labelled green bonds issued in H1 2018 were analysed.

- 11 out of 28 issuers are first time green bond issuers. TenneT issued two green bonds, alongside NAB (Certified Climate Bond), the Kingdom of Belgium and Enel as other prominent examples.

- Green bonds achieve greater spread compression, and larger book cover during pricing than vanilla equivalents on average.

- Green bonds in H1 2018 priced either outside or on their yield curves.

- 55% of green bonds were allocated to investors declaring themselves green, the most we have seen so far. Non-mandated investors continue to support the market.

- Green bonds tend to tighten more than vanilla benchmarks in the immediate secondary market.

- Green bond issuers continue to extol the virtues of going green.

- Spotlight on investment grade Emerging Market green bond issuers.

Detailed Findings:

- Q1 2018 is the first period in which green bonds have performed better than vanilla equivalents in both EUR and USD in terms of having larger book cover and greater spread compression. 17 out of 23 EUR green bonds, and 6 out of 6 USD bonds had larger oversubscription than vanilla equivalents. Average spread compression was also larger for vanilla equivalents.

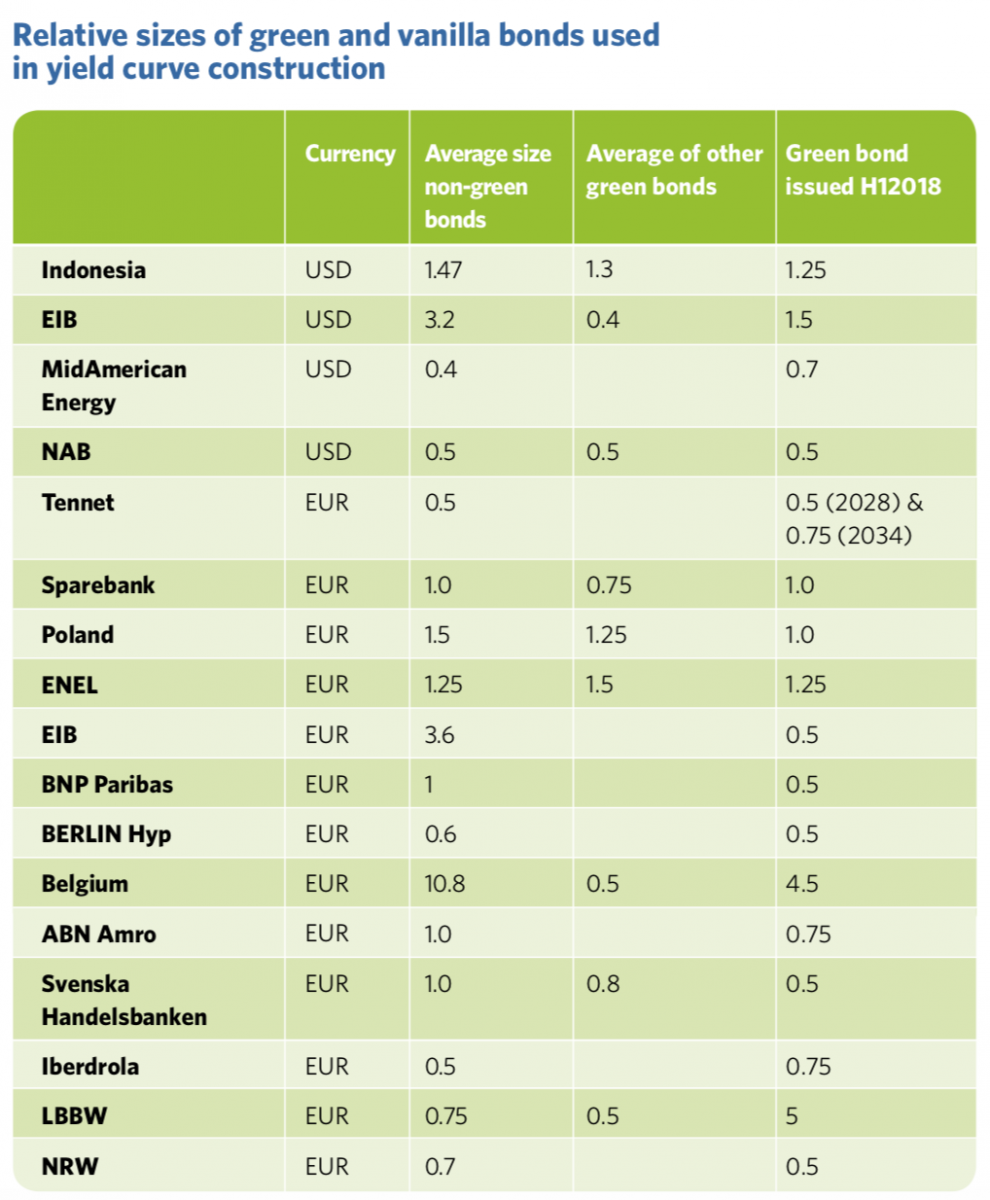

- CBI built yield curves for 17 out of 28 issuers. Five bonds priced on the curve, 12 exhibited traditional new issue premia. Five bonds in our sample had secondary market green curves in addition to vanilla curves.

- Green bonds continue to attract a broad range of investors. 55% of green bonds were allocated to green bond investors, the highest percentage we’ve seen so far. This suggests that the pool of dedicated green bond investors is growing.

- Green bonds appear to have performed well in the immediate secondary market. More green bonds tightened by a larger percentage compared to comparable indices and baskets of vanilla bonds than did not, after both 7 and 28 days.

- Aside from pricing, green bond issuers highlight other clear benefits including a diversified investor base and enhanced visibility for corporate and social responsibility initiatives.

Special Section on Emerging Markets

We took a closer look at USD80.47bn of qualifying green bonds issued from Emerging Markets between January 2016 and June 2018. An overwhelming 93% of this debt was denominated in CNY, USD, and EUR. During this same period, a further USD25.9bn was also issued from supranational development banks.

Most of the proceeds raised would have also been directed into emerging markets including those having insufficient credit status to raise and manage money directly. The most prolific domiciles for EM green bonds to date have been China (Moody’s: A1 / S&P: A+), Mexico (Moody’s: A3 / S&P: BBB+), and India (Moody’s: Baa2 / S&P: BBB-).

We are continuing to monitor EM pricing and will report on a larger sample size in our next iteration.

Who’s saying what?

Peer Stein, Global Head of Climate Finance, Financial Institutions Group IFC:

“IFC estimates that the Paris Agreement commitments represent $23 trillion in investment opportunities by 2030, and Green Bonds hold great promise as a way to finance them. Pricing and investor trends for emerging markets’ green bonds seem to be aligned with the global green bond trends, though more data and research is needed."

"IFC would also like to see more investor diversification, as the share of dedicated green bond investors participating in emerging markets green bond issuances is lower than for developed market issuances. This is clearly an area for future growth.”

Sean Kidney, CEO, Climate Bonds Initiative:

“The analysis points to another sign of wider market interest in quality green product. This is reflected in pricing signals, on top of the anecdotal evidence from individual issuers. It’s still early days for positive pricing of climate factors in most investment products.”

"We expect, as the green bond market develops towards its first trillion, that pricing trends will become more visible."

"In 2018 we’ve moved to a semi-annual reporting cycle that reflects a longer-term perspective on what is a dynamically evolving market. Twice yearly analysis on larger data sets matches more closely with the needs of the growing number of issuers and investors, looking to hedge growing climate risks and take the long-term opportunity that exposure to green assets will provide.”

The last word

Market appetite for green bonds is reflective of the pricing trends and larger book cover. Issuers see other benefits as a result of green issues, a greater focus by the market on issuer’s green initiatives including ESG and alignment with climate outcomes.

We will continue tracking pricing trends twice every year as the market moves further into the hundreds of billions in annual issuance. Keep an eye out for our next update covering Q3-Q4 (H2) 2018, due for publication in April 2019.

‘Till next time,

Climate Bonds

Methodology for the report:

This paper includes labelled green bonds issued during H1 2018. We have included all labelled green bonds meeting the following specifications:

This paper includes labelled green bonds issued during H1 2018. We have included all labelled green bonds meeting the following specifications:

-

Announcement date between 01/01/2018 and 30/06/2018

-

Currency: USD or EUR

-

Size >= USD500m

-

Investment grade rated

-

Minimum term to maturity of three years at issue

-

Consistent with Climate Bonds Taxonomy

- Amortising, perpetual, floating, and other non-vanilla structures are excluded.

We have designed these parameters to capture the most liquid portion of the market, while not limiting diversity. Paucity of data remains a challenge. All historical data is based on asset swap spreads for EUR denominated bonds. For USD bonds, spreads are against a US treasury curve. All historical data is taken from Thomson Reuters EIKON.

Comparable baskets:

Comparable baskets include bonds issued in the same quarter as the green bond. Comparable bonds must fit the parameters described above except that the use of proceeds is not green. The resulting baskets are a proxy for how the money could have been invested within a three month period. The number of bonds in each basket ranges from one to 11 bonds. We acknowledge that bonds behave differently according to which part of the month they are issued in, and that geopolitical events can influence bond prices from one day to the next. We have designed this proxy to circumvent the fact that green and vanilla bonds sharing similar characteristics are rarely issued on the same day.

Ackowledgements: Green bond pricing in the primary market January-June 2018 was prepared jointly by the Climate Bonds Initiative and the International Finance Corporation (IFC).

Support and funding was provided by Impax World Mutual Funds and Obvion Hypotheken. Additional funding was received from the Ministry of Finance of Japan and the Government of the Kingdom of Denmark through the Ministry of Foreign Affairs.

Previous Pricing Reports:

- Green Bond Pricing in the Primary Market: Q4 2016 Snapshot can be found here.

- Green Bond Pricing in the Primary Market: Jan 2016 – March 2017 can be found here.

- Green Bond Pricing in the Primary Market: April – July 2017 can be found here.

- Green Bond Pricing in the Primary Market: July – September 2017 can be found here.

- Green Bond Pricing in the Primary Market: October – December 2017 can be found here.